.svg)

.png)

Data center powering models: How the AI boom is reshaping power demand and generation

.png)

The AI race — to train larger models, deploy faster inference, and corner market share — has triggered a parallel arms race for electricity. You’ve likely seen the “up and to the right” AI-related load growth charts: the IEA projects global data center electricity consumption will climb by ~15% between 2024 and 2030. McKinsey forecasts a 3.5x increase in data center capacity demand in just five years (2025–2030). It's the first meaningful growth in electricity demand in developed economies in decades.

But now the name of the game for development is how to get power ASAP. It's become the greatest bottleneck and the first priority in site selection. Sightline's new report takes on these top-down projections and trends with a bottom up approach to see out what’s really happening on the ground. We've got the dataset tracking actual data center developments, their proposed powering models, and the grid plans (or lack thereof) to bring them online. These are the real demand signals that utilities, developers, and tech companies are trying to plan around.

You can download the full report and get exclusive data, charts, and regional breakdowns inside the full Sightline Climate Data Center Powering Models (August 2025) report — including case studies, cost benchmarks, and powering strategies from global developers 👉 Access the full report on Sightline Climate.

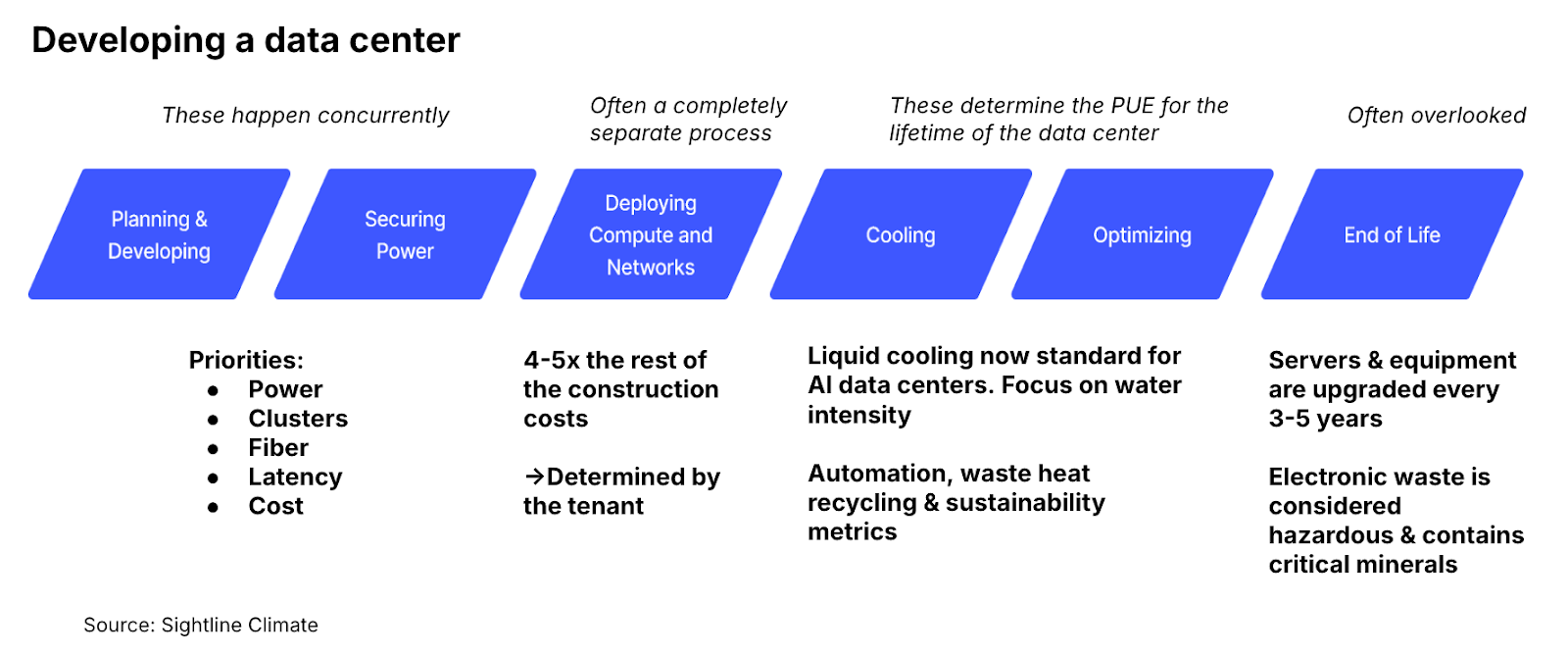

Power first, everything else second

For most of the cloud era, data centers were built where latency and fiber connectivity were best — near cities and internet exchanges. That logic is breaking. Today, the first question any developer asks is simple: Where can I get firm power, fast?

Utilities and grid operators are caught in the middle — squeezed between surging demand from tech giants looking to develop sites ASAP and regulatory pressure to keep the lights on and rates affordable. There’s opportunity here (data center demand can accelerate clean generation) but also risk: overloaded interconnection queues, community pushback over higher rates, and the specter of stranded assets.

Inside the powering models behind the boom

.png)

Powering strategies break down into two main categories: on-grid and off-grid, with varying mixes of clean and fossil generation, each with trade-offs.

- On-grid models offer balancing and reliability but face 5–10-year interconnection waits.

- Off-grid setups — small turbines or microgrids — are faster to build but complex and costly to manage for 99.999% uptime.

- Hybrid models blend both, using backup power to bridge the gap until grid supply arrives.

Clean, fast, cheap, and firm is the “Goldilocks” combination every operator wants, but only a handful of sites can deliver all four. Developers end up compromising: paying more to get clean, or burning gas to get fast.

Backup power plays a starring role. Most new facilities are built with large gas or RNG turbine systems that can run the entire campus if needed. Batteries aren’t enough; they still depend on the grid to recharge.

Tariffs and the quest for clean firm power

In the US, large data centers fall under “large load” tariffs that lock in long-term capacity and pricing. These agreements de-risk new generation by requiring exit fees, minimum loads, and sometimes direct investment in substations or low-income offsets.

A new generation of clean power tariffs is emerging:

- Nevada’s Clean Transition Tariff (CTT)

- North Carolina’s Green Source Advantage Choice

- Duke Energy’s Accelerating Clean Energy (ACE) program

These give hyperscalers a path to clean, reliable power while shielding ordinary ratepayers from cost spikes.

Utilities are also experimenting with “interruptible service” connections — faster hookups that let operators agree to short power curtailments during grid stress. It’s not ideal for all workloads, but it can shave years off connection timelines.

Gas: the fast and familiar bridge

In the near term, natural gas remains the fastest route to power. Small turbines can be installed in months and run independently of the grid. Many developers tout them as “hydrogen-ready” or CCS-compatible.

But according to Sightline, Gas + CCS (carbon capture and storage) is still limited to Texas, Wyoming, and the Midwest — regions with existing CO₂ transport and storage networks. Projects elsewhere face long permitting times and uncertain economics. Even in ideal locations, full systems can take five to seven years to deliver.

For now, most sites start with unabated gas, planning to retrofit carbon capture or offset emissions later. Sightline notes that only one significant gas+CCS pilot — the Bellingham plant — has operated at scale.

Geothermal, nuclear, and other long-term bets

Clean firm power is the endgame. The report highlights three emerging models:

- Geothermal — Firms like Fervo and Eavor are bringing advanced drilling to new regions. Power purchase agreements already range from $77 to $202 per MWh, with one Fervo–NV Energy deal at $107/MWh. Best suited for the western and southern US, geothermal aligns naturally with next-gen data center clusters in Nevada, Wyoming, and Texas.

- Small Modular Reactors (SMRs) — Tech companies are exploring colocating data centers with future SMRs. Clean, dense, and reliable, but 10+ years out and facing long regulatory queues.

- Restarting retired nuclear plants — A few developers are evaluating whether decommissioned nuclear sites could be revived with private investment, taking advantage of existing transmission infrastructure.

Each model is slower to build than gas but adds genuinely new, additive clean power to the grid.

The global buildout — and the numbers behind it

In Sightline’s dataset, we’ve tracked 294 data center projects weighing-in at 73.6GW demand, of demand, as of June. (These numbers are updated monthly for clients.) The pipeline is constantly evolving with new projects announced basically every day — we’re tracking those too.

.png)

Over 8.9GW across 105 projects in the pipeline are targeting operation by end-2026, with 47 already under construction.

The US leads with 106 sites, followed by large clusters in Europe and Asia. The UK’s 1 GW Northumberland project and France’s NVIDIA AI Factory alone will increase national capacity by 63% and 145%, respectively.

Big Tech dominates the leaderboard: Microsoft (21 projects), Google (19), Amazon (18), and Meta (12). But governments are also scaling up — the US DOE (16) and EU EuroHPC JU (11) are funding national compute projects to stay competitive.

Investment drivers include:

- Use case: AI-optimized facilities are 5–6x more capital intensive than standard cloud sites.

- Location: Urban proximity raises costs; rural sites face grid buildout delays.

- Build type: Retrofit vs. new-build drastically affects cost, timeline, and grid integration.

The economics: expensive, uneven, and accelerating

Building data centers remains capital-intensive — and unpredictable:

- Median project investment: ≈ $800 million

- Average cost: ≈ $5.5 million/MW

- AI-specific facilities: 5–6× more expensive than traditional colocation centers due to GPUs and liquid cooling

- Retrofits: ≈ 35% cheaper than greenfield builds

- Full-stack power setups: High upfront costs, but avoid grid delays and price volatility

Location matters. Urban and high-wage regions like Northumberland or South Korea face steep costs, while emerging markets such as Malaysia are cheaper but riskier on power reliability.

Recommendations: what comes next

Sightline closes the report with pragmatic advice for each stakeholder group:

For data center developers

- Bring your own generation. Utilities prefer projects that add capacity rather than just consume it.

- Invest in robust backup systems. They speed up grid approvals and can even generate revenue through flexibility services.

- Work with experienced utilities. Those with data-center-specific tariffs can shorten permitting and connection times.

For utilities and power producers

- Highlight regions with spare capacity. Pairing ready-to-go power with clear permitting paths attracts development.

- Offer interruptible connections. Many AI workloads can handle controlled outages.

- Strengthen local distribution grids. Smarter substations and automated restoration will be key to reliability.

For policymakers

- Streamline permitting in areas with excess or underutilized generation.

- Mandate low-carbon backup systems in congested regions to reduce strain on local grids.

- Use incentives and tax credits to encourage long-term clean generation tied to data center growth.

The next decade of data center growth will be defined by who can secure clean, firm, and affordable energy fast enough to keep AI scaling — without overwhelming already-strained grids.

👉 Get the full Data Center Powering Models report here.

FAQs

1. How much power do data centers consume globally?

As of 2022, ~460TWh annually — about 2% of global electricity usage. That number could grow 50–150% by 2030.

2. What’s driving the surge in demand?

AI training and inference workloads, hyperscale cloud growth, and digital infrastructure expansion, among other factors.

3. Why is power availability now the top siting factor?

Latency used to matter most. Today, megawatts — not milliseconds — are the gating factor for development.

4. What are the main powering options?

Gas turbines, renewable microgrids, grid tie-ins, repurposed coal connections, and long-term bets like SMRs and advanced nuclear.

5. Which regions are leading in data center buildout?

The US leads capacity, but Europe, Asia, and MENA are accelerating due to AI strategies and grid constraints in the US.

6. What’s the average size of new projects?

150MW was big a few years ago. Now 1GW is common, with some exceeding 3GW.