.svg)

.png)

H1 2025 climate tech investment: Capital stacking up for energy security & resilience

.png)

Today, we’re releasing Sightline’s H1 2025 Climate Tech Investment Trends report — your recap of the funding, deal flow, exits, and investor activity through the first half of the year.

As we said at the end of 2024, climate tech is settling into its new normal after funding froze. 2025 hasn’t exactly thawed out so far, but at least it’s not getting colder.

In H1’25, funding dropped 19% — a smaller dip compared toH1’23’s 41% plunge, but we wouldn't call it a comeback (yet). We're calling this the end of the “see” in wait-and-see. Five to seven years into the current cycle, LPs are waiting for exits and liquidity. There haven't been many to find.

But beneath the cooling headlines, a new investment thesis is heating up.

Rising protectionism is making access to domestic energy, critical minerals, and stable infrastructure a strategic priority. At the same time, with warming surpassing 1.5°C and climate impacts becoming harder to ignore, resilience is increasingly investible. Add the rearranging macro elements — weaker subsidies, shifting trade precedents — and the market doesn't want green premiums anymore. They want green discounts. As Carlyle's paper, the New Joule Order, highlights, this may not be a bad thing: a security lens could even lead to higher returns and a faster transition.

In H1’25, we saw this play out across multiple fronts:

- Mega-deals in nuclear, critical minerals, and SAF show growing momentum behind technologies that anchor domestic supply chains, boost reliability, and reduce dependence on volatile imports.

- Gridtech posted its best quarter ever, hitting $316m in Q1 alone amid rising climate risks, aging grid infrastructure, surging AI power demands, and the electrification of everything.

- Climate management funding jumped 19%, as investors backed platforms monitoring oceans, forests, and risk exposure — tools that support both climate adaptation and resilience.

And beneath it all, like this thesis, the capital stack is adapting. There are still surprises, some good news, and plenty to watch in the second half of this already-turbulent year.

We’ve rounded up the charts, trends, and takeaways below. Dig into the full report here.

Sightline clients can access the report, complete with deeper deal data, vertical breakouts, sector-by-sector breakdowns, exits analysis, and a data pack, on the platform here.

Takeaways

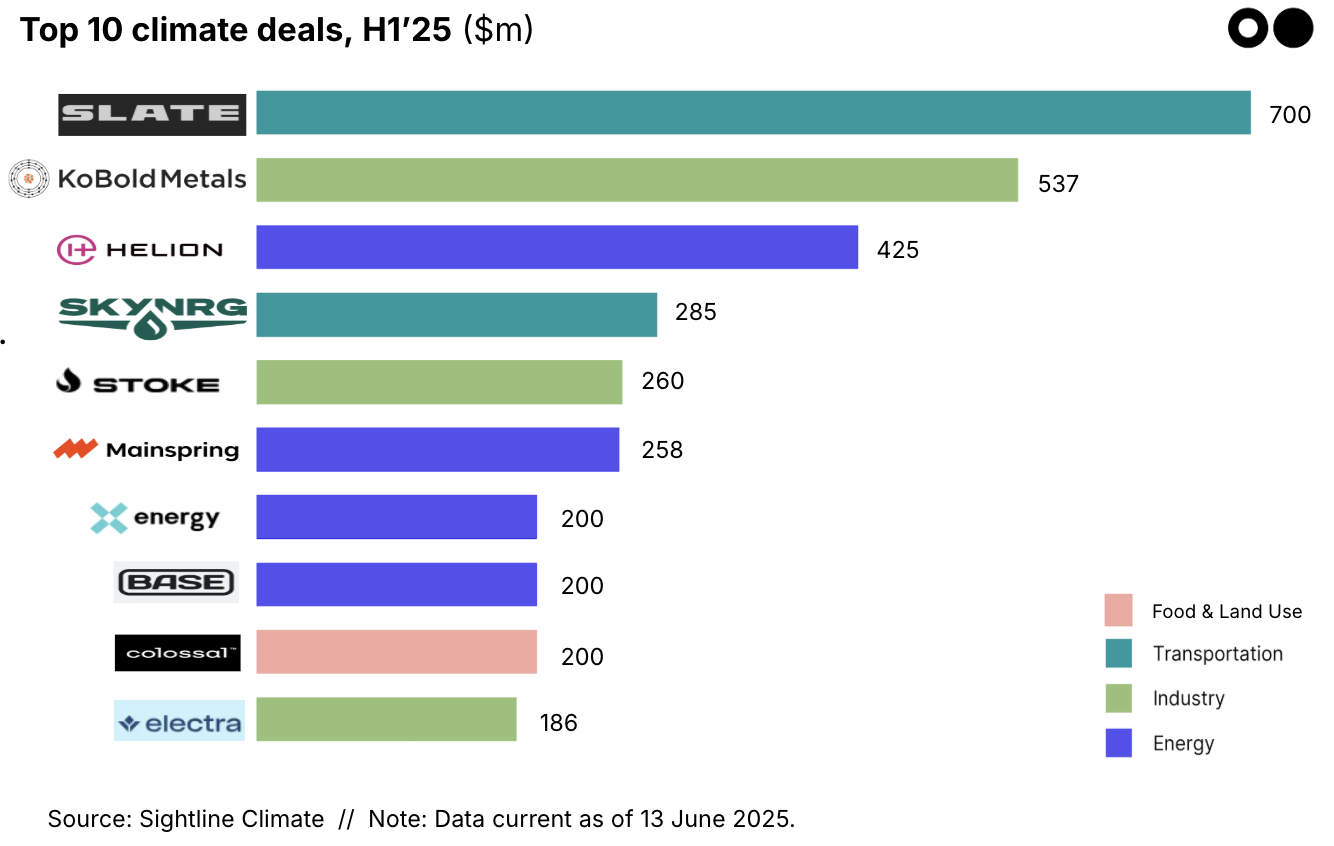

🎯 Security, adaptation, and resilience front and center: Mega-deals are increasingly tied to energy security and adaptation, with nuclear, space, critical/strategic materials, and even de-extinction featuring in the top 10.

🇪🇺 Europe’s sentiment vs. reality: Investor optimism for Europe remains high, but the numbers tell a different story. US investment grew 21% in H1’25 compared to H1’24, while Europe dropped 51%. Deal counts are nearly identical (259 in the US vs. 248 in Europe), but mega-deals are keeping the US well ahead. Expect Europe to catch up in project deployments and late-stage financings over the next few quarters — for now, US companies still dominate on capital raised.

🏭 Industry’s steady funding is a quiet win: Historically, industry has drawn patient capital for large-scale assets and hardware. In today’s leaner, asset-light climate, that approach faces headwinds. Against that backdrop, holding funding steady is an achievement in itself.

🚪 Exits — or lack thereof: SPACs have made a comeback in areas like SAF and SMRs that aren’t yet commercial, but traditional IPOs remain rare outside India. M&A activity, however, is ramping up — acquisitions doubled vs. H1’24. Bankruptcies slowed but still hit hard, with companies like Northvolt, Sunnova, and Li-Cycle succumbing to policy shifts and post-ZIRP macro pressure. Many smaller firms unable to raise are fading quietly. Expect further consolidation ahead.

Scroll on for a few key numbers — but download the full report for more analysis and what it all means for the rest of 2025.

Highlights

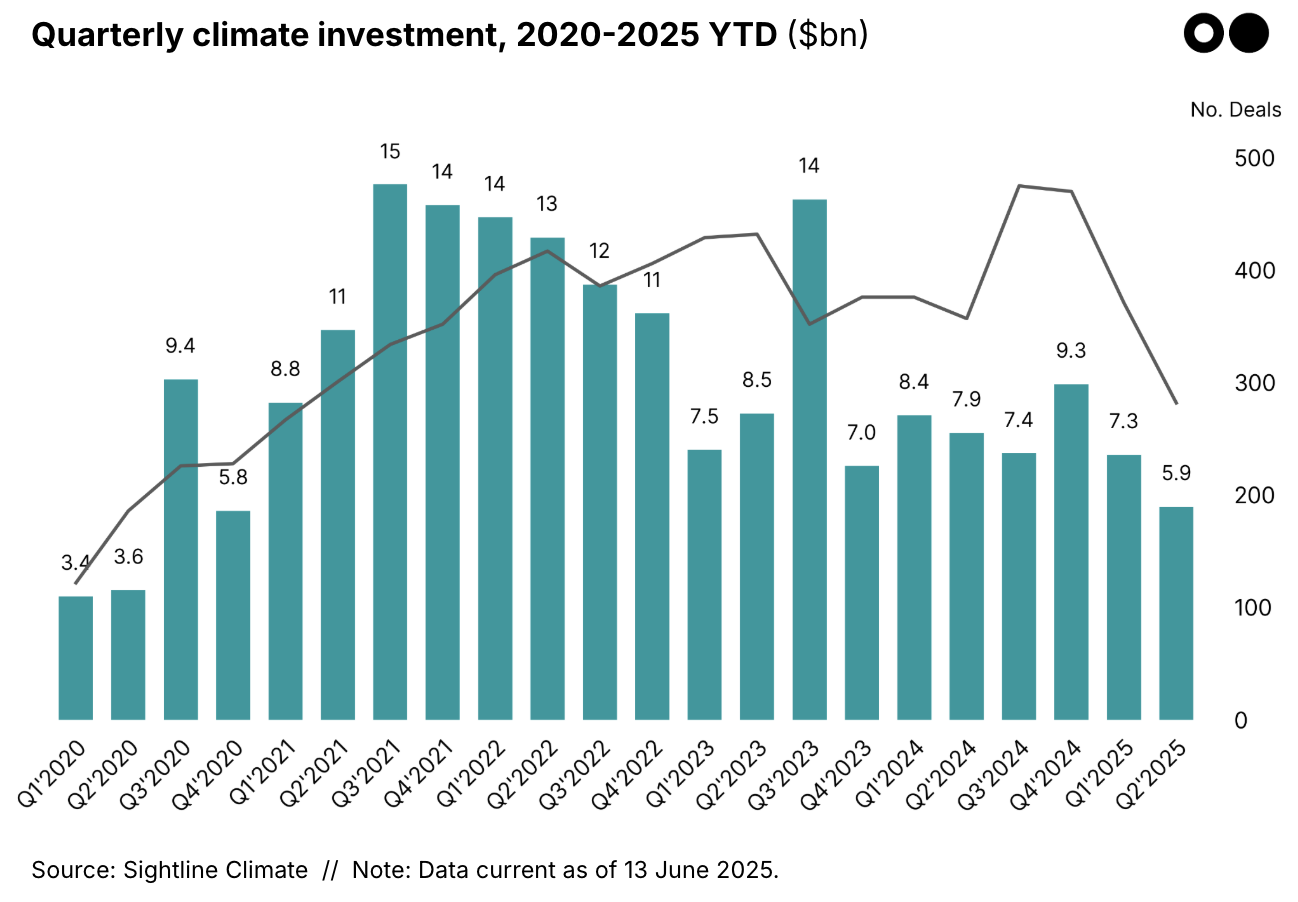

💰 H1’25 funding: Climate tech venture and growth investment totaled $13.2 billion in H1’25, down 19% from H1’24, and 17% from H1’23. There were 653 deals in H1’25, 11% less than in the first half of 2024.

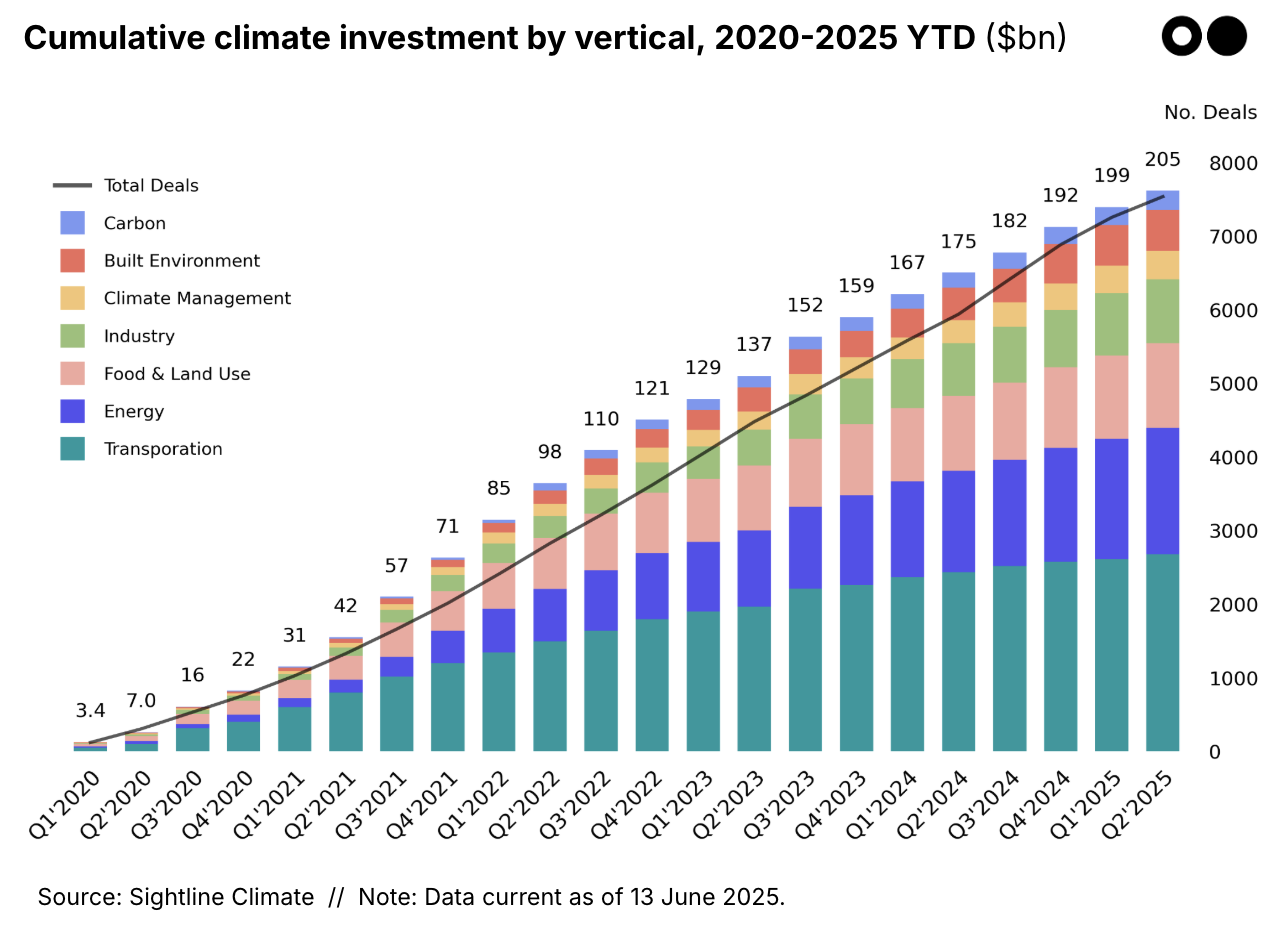

📈 Cumulative growth: H1’25 increased cumulative investment since 2020 by 7% to $205 billion, but that growth is marching along at a slow and steady pace, compared to 10% growth in H1’24 and 13% in H1’23. Notably, quarterly growth is decelerating too. It was just 3% in Q2’25, down from 5% last year and 7% the year before.

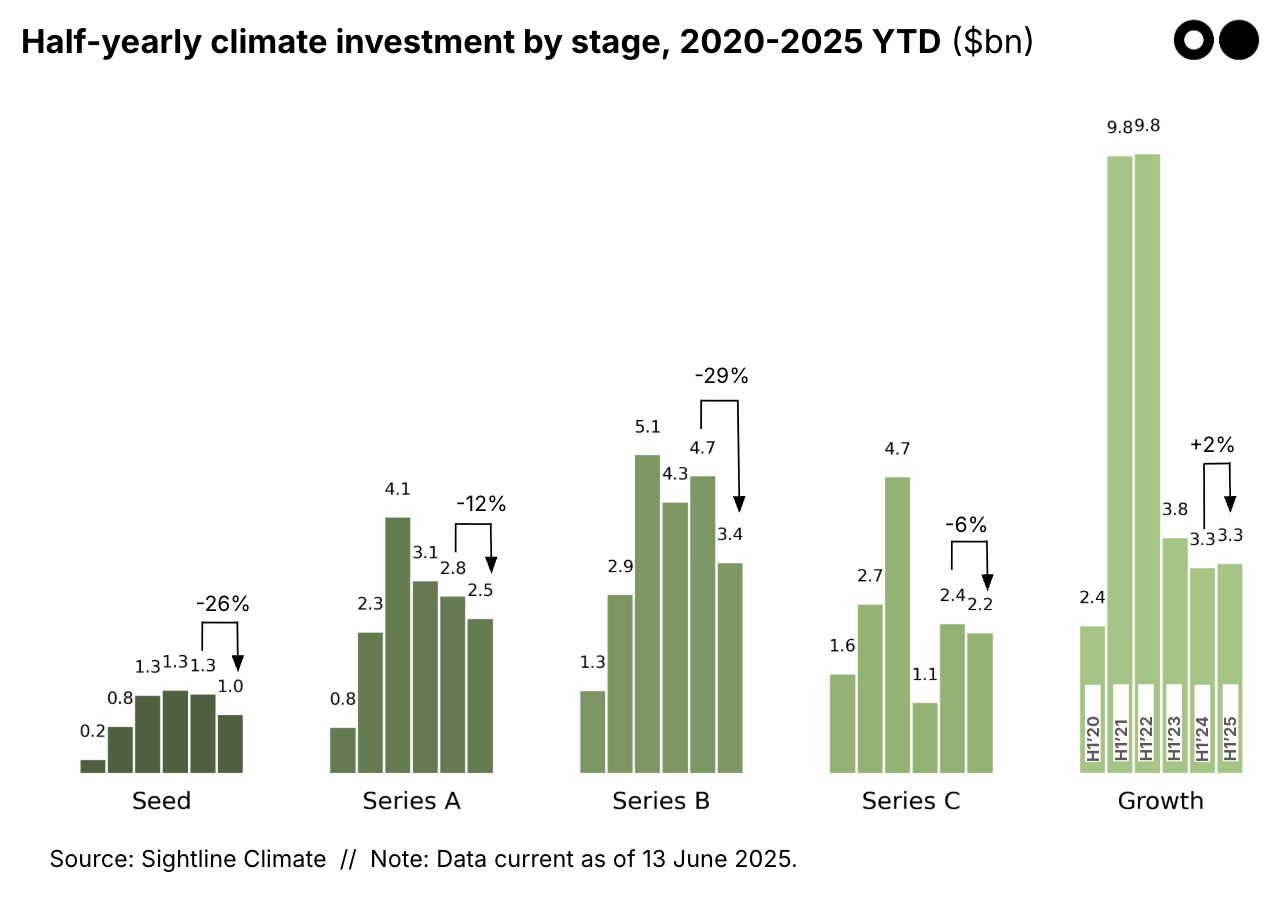

📉 Stage: Funding declined across nearly all rounds, with Series B taking the sharpest hit, down 29% from H1’24. Seed wasn’t far behind, falling 26%. Later stages, however, proved more resilient: Series C dipped only 6%, while Growth edged up slightly, buoyed by mega-deals in fusion and low-carbon fuels.

🤝 Top deals: Of the $3.3 billion in mega-deals, $2.3 billion—and eight of the top ten—centered on security, resilience, and adaptation. Highlights included investments in advanced nuclear power (Helion, X-energy), critical minerals supply (KoBold, Electra), and space (Stoke). The average size of the top 10 deals was 31% higher than in H1’24.

⚡ Vertical: Energy once again led the pack, capturing 35% of H1’25 funding. The sector grew 13% to reach $4.6 billion, with fusion overtaking energy storage as the second-largest category. At the same time, earth observation funding surged, reflecting renewed momentum around climate adaptation.

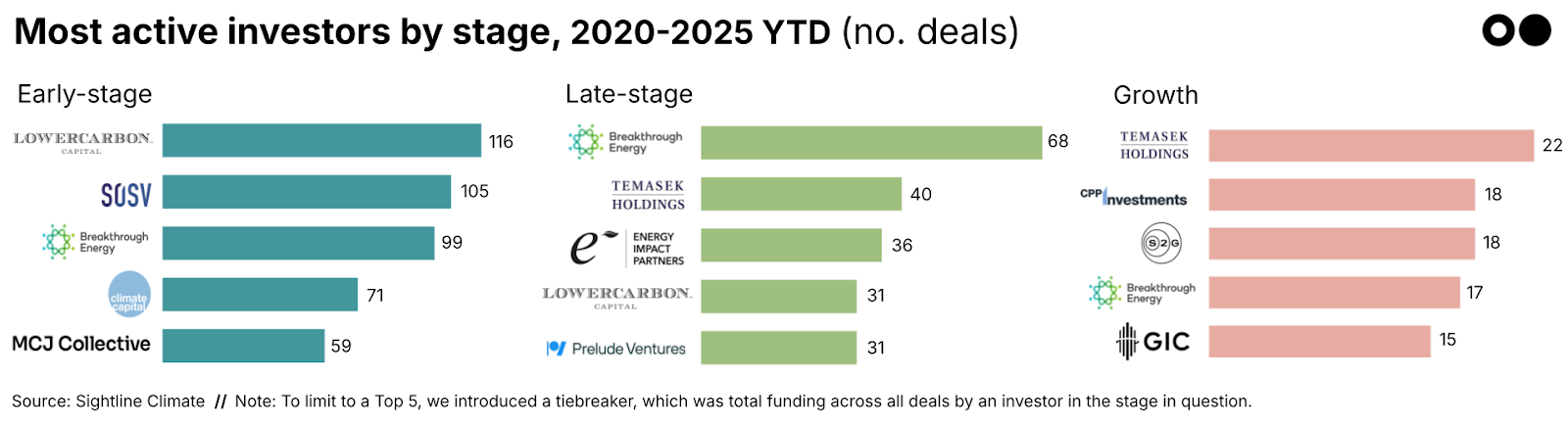

👔 Investors: The roster of leading climate investors remained largely stable, as specialist firms doubled down with follow-on investments and held onto the deal count advantage they built during the 2021–2022 surge. Still, a few shifts stood out: S2G edged Goldman Sachs off the Growth leaderboard with new bets in agri-fintech and ocean data, while Lowercarbon’s run of Series B deals pushed it further into later-stage territory.

Click and access the full report here.

Methodology

This funding report captures only Venture Capital and Growth Equity deals that have been publicly announced through regulatory filings or press releases as of June 13, 2025. Read more about methodology and definitions in the methodology section of the full report.

NOTE: You may notice that some of our numbers are larger in this update than previous editions. We constantly update the dataset to have the most accurate data possible, including adding post-dated deals.