.svg)

.png)

Understanding Sightline's Sector Readiness Curve

Novel energy and climate solutions are moving from innovation to deployment. As tech is de-risked and the markets mature, they start to approach scale and the almighty exponential curve. At least, that was the narrative of solar and wind racing down cost curves, batteries beating expectations, EVs moving from niche to mainstream.

But inside the scale up, things don’t look quite as linear. Technologies that once looked unstoppable can run headlong into financing gaps, permitting roadblocks, or demand that fizzles out. Others, written off for decades, can suddenly gain traction as breakthroughs align with market needs. For every sector that accelerates, another stalls, and some can even slip backwards on the path to scale.

Today, a new wave of technologies is approaching scale — from direct air capture to sustainable aviation fuels, advanced geothermal, hydrogen, and beyond. But they haven’t reached escape velocity yet. They have their own hurdles: massive supporting infrastructure requirements, lagging interconnection times, and an uncertain policy landscape.

That volatility leaves corporate strategists, innovation leaders, investors, and bankers with the same gnawing question: what’s real, what’s ready, and what’s still just noise?

Why a new framework is needed: Introducing the Sector Readiness Curve

Policymakers and academics have long relied on tools like Technology Readiness Levels (TRLs) to evaluate new solutions. TRLs are useful — but too narrow. They track whether a technology works, not whether it can scale. In the market, that’s only one piece of the puzzle.

Over the past three years, in conversations with hundreds of capital allocators, developers, and corporate teams, a pattern became clear. Success or failure doesn’t hinge on technology alone, but on a web of interdependent factors: financing, buyers, supply chain players, cost competitiveness, and policy. Each dimension has the power to pull a sector forward — or hold it back.

That recognition led us to build the Sector Readiness Framework – a simple yet powerful way to track commercialization momentum. It’s simple enough to use in the boardroom, but powerful enough to explain the messy, uneven paths technologies actually take on their journey from lab to market.

It underpins how Sightline thinks about its research, data, and tools.

Building the curve, step by step

Technology: Is the technology de-risked?

Every sector journey starts with the same question: can this technology work outside the lab? Without credible performance in the real world, nothing else matters.

Fusion is the quintessential case. Investors have poured in billions, scientific breakthroughs keep making headlines, and politicians eagerly promise a future powered by limitless clean energy. But fusion hasn’t delivered a single commercial electron to the grid. Technical reliability remains the bottleneck.

.png)

At the other extreme sit EVs and lithium-ion batteries. A decade ago, they were unproven and expensive. Today, they’re commercial workhorses, competing head-to-head with incumbents on both cost and reliability. It shows how readiness can shift rapidly once technology risk is solved.

Technology maturity is the gatekeeper. Without it, no amount of finance, demand, or policy will matter. But once credibility is established, the rest of the readiness curve comes into play.

Finance: Is the capital stack there?

If technology maturity sets the floor, finance builds the bridge to scale. But that bridge is often missing for first-of-a-kind projects.

Pilots can be funded with venture dollars, and project finance steps in once the tech can be deployed commercially. But the FOAK scale — $50m to $500m projects — is too large for venture and too risky for banks. That’s the infamous “missing middle.”

Take carbon removal. Startups attracted venture funding and corporates like Microsoft signed on for early purchases, but billion-dollar FOAK plants aren’t fully funded. The tech works in principle, yet scaling risks — construction delays, supply chains, shaky unit economics — keep lenders away.

.png)

Some sectors are finding creative ways through. In SAFs, airlines have signed long-term offtake agreements that give projects the bankable demand streams needed to unlock financing. It’s an early template for bridging the FOAK gap.

Demand: Who’s buying? Who will pay for it?

Even if financing is available, scale doesn’t happen unless buyers show up.

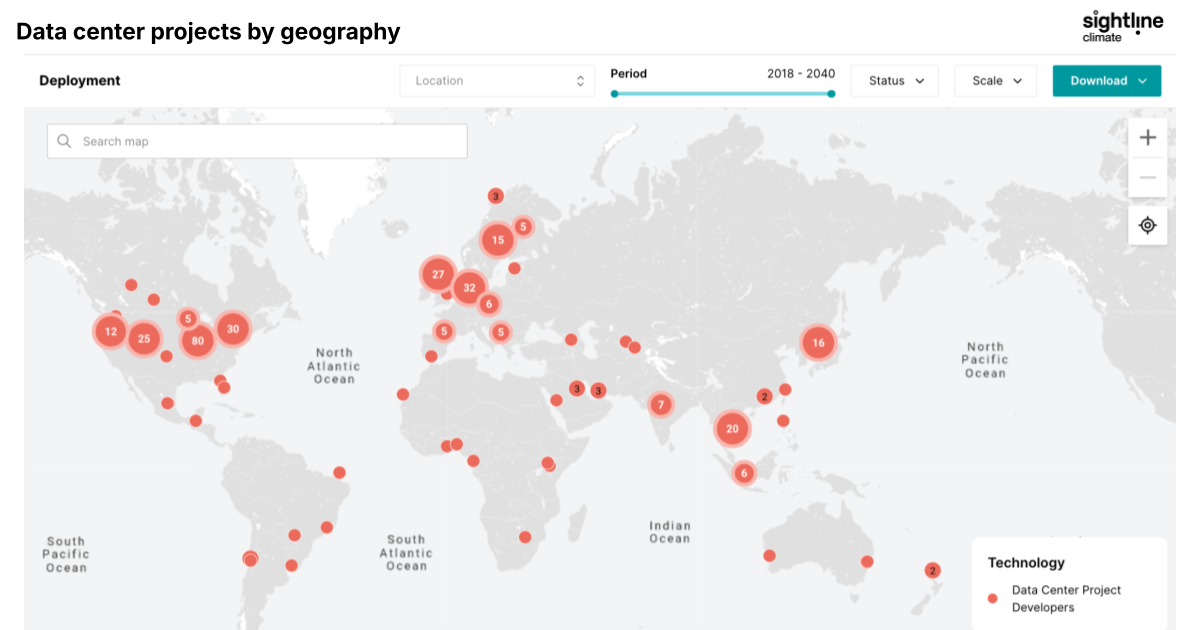

Hyperscale data centers are playing a similar role to SAF offtakers, as mentioned above, in power markets. As AI and cloud demand surge, operators like Microsoft and Meta have signed multi-gigawatt PPAs across renewables, nuclear, and geothermal. These deals are shaping investment decisions across entire grids.

Without credible buyers, no sector can cross the readiness curve. Even with capital, scale depends on certified demand.

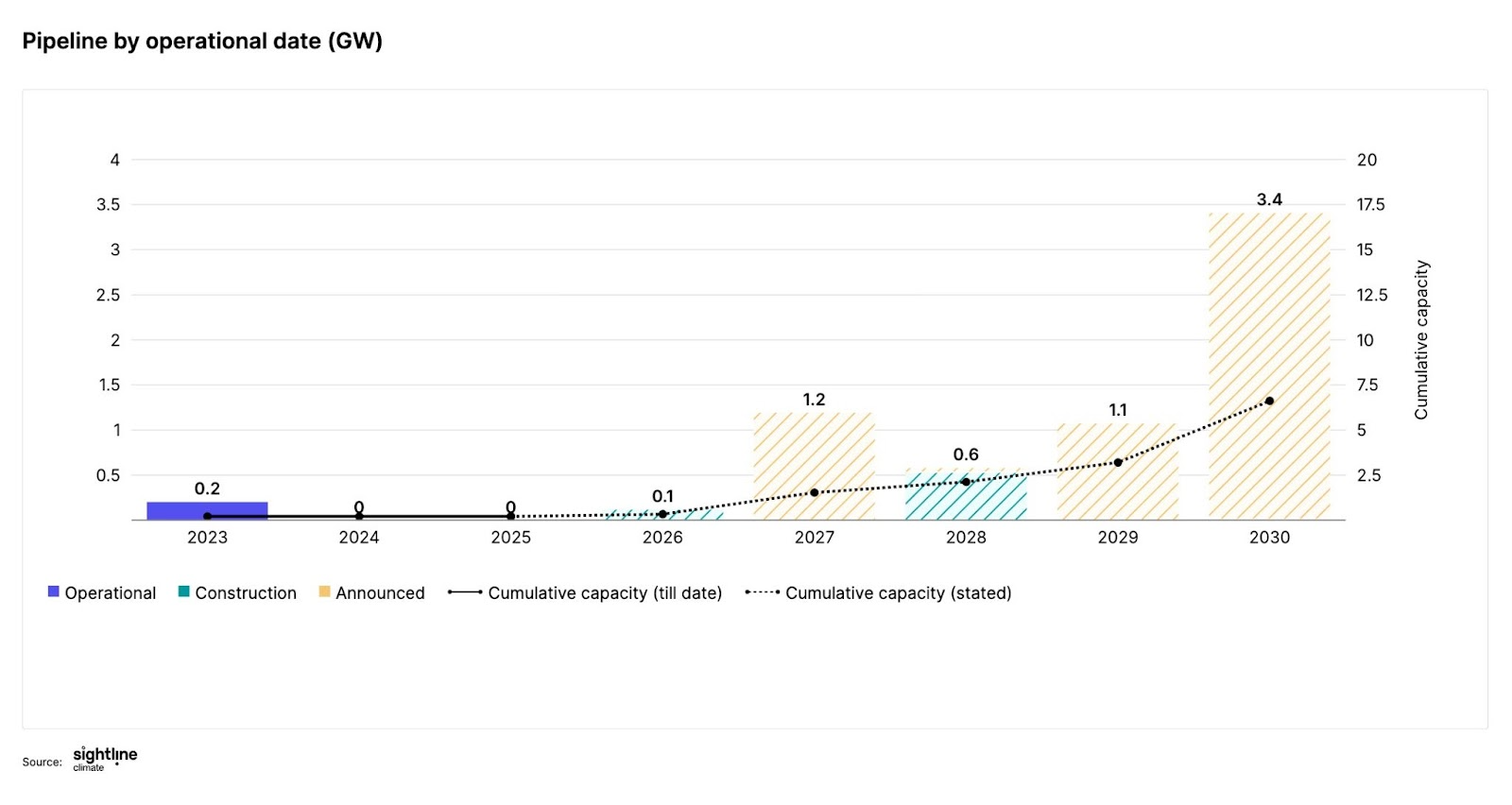

Deployment: Are projects getting built?

Deployment is where promise meets reality. Announcements are cheap. Construction is expensive.

Emerging clean firm power sources, from fusion to advanced geothermal and advanced nuclear, have been steadily progressing in deployment. You can see the growing pipeline of projects moving from design into construction. Each new plant helps validate the technology for utilities and financiers, creating a domino effect of credibility.

Nuclear small modular reactors, on the other hand, have captured headlines for a decade. Yet few projects have broken ground, and high-profile cancellations show how fragile deployment momentum can be.

Players: Is there an ecosystem?

Technologies don’t scale alone. They need an ecosystem — developers, suppliers, and incumbents with the balance sheets and distribution networks to make it real.

In EV charging, that system is clear. Hardware makers like ABB and Wallbox, software platforms, utilities, and turnkey operators each play a part. No one controls the market, but together they create the scaffolding for rapid deployment.

.png)

Heavy industries are tougher. Cement and steel remain dominated by entrenched incumbents. Startups can’t scale without partners like Holcim, Heidelberg, or ArcelorMittal — and they usually act only under regulatory pressure. (That’s why most low-carbon cement projects are in Europe, where carbon pricing and CBAM make the business case.)

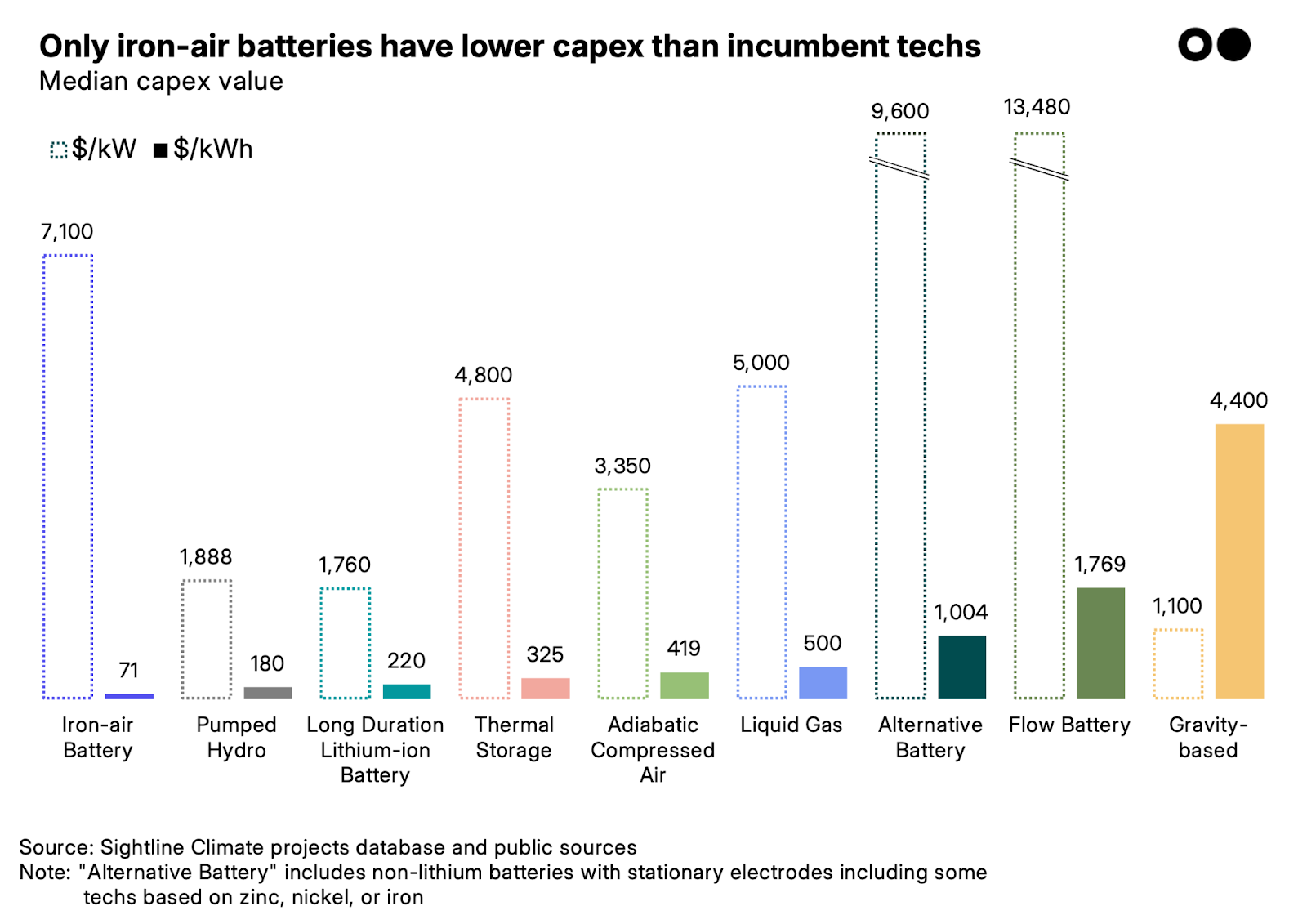

Economics: Is it or can it get to cost parity?

Cost competitiveness is the endgame, the holy grail. Technologies may advance, financiers may experiment, and buyers may sign early contracts, but without economics on their side, they can’t sustain the momentum.

LDES, despite its theoretical advantages — cheap materials, onshored supply chains, and “decoupled power and energy” — still costs far more than the simpler workaround of derating a 4-hour lithium-ion BESS to lower power output. That incumbent “long-duration lithium-ion” solution benefits from existing economies of scale.

The economics dimension is unforgiving. Technologies either reach cost parity or risk being stranded.

Policy: Is there a carrot or a stick?

Finally, policy can tilt the playing field. Subsidies, tax credits, and regulatory sticks accelerate some sectors while stalling others.

In the US, the IRA reshaped entire markets, offering $3/kg for clean hydrogen, $85/ton for CCS, and $180/ton for DAC. These incentives were set to bring projects forward years ahead of schedule. But reversals in the One Big Beautiful Bill are hitting the brakes, and causing some technologies to slide backwards in their readiness. Brimstone’s $189m DOE loan guarantee was pulled in 2024, leaving its first cement plant scrambling to fill a $289m funding gap. Government tailwinds can vanish overnight, leaving companies exposed.

In Europe, the EU ETS and CBAM are forcing cement and steel producers to act. At carbon prices of €60/t, cement costs would rise by as much as 40%. That shifts climate tech from optional to existential.

This is policy being used as a catalyst, but it’s not one that decision-makers can rely on indefinitely.

The Sector Readiness Curve

Individually, these dimensions are powerful signals. Put these dimensions together — Technology, Finance, Demand, Deployment, Players, Economics, and Policy — and you have the Sector Readiness Curve, Sightline’s proprietary framework for commercialization readiness.

- Technology – maturity and reliability

- Finance – availability of capital and structures

- Demand – committed buyers and offtakes

- Deployment – projects coming online

- Key Players – scaled incumbents and ecosystem partners

- Economics – cost parity and scale effects

- Policy – incentives and regulations shaping uptake

.png)

Why it matters

For strategists, innovation leaders, business development directors, and capital allocators, the Sector Readiness Curve is more than a framework. It’s a way to monitor the state of markets and understand their trajectory — and can even be applied in mature sectors like solar, wind, storage, and EVs. Reaching cost parity doesn’t mean technological progress, deployment, or demand don’t matter, especially in increasingly competitive markets.

The framework helps decision-makers navigate macro uncertainty. It guides strategists on which markets to prioritize, helps innovators separate hype from credible solutions, and enables BD teams to time outreach for when prospects are truly ready. For investors and bankers, it clarifies when sectors cross from venture bets into infrastructure plays. More than a theory, the Sector Readiness Curve is a practical tool for making better decisions and doing the work.

- Strategy: Prioritize which markets to enter, which technologies to back, and which partners to pursue.

- Innovation: Separate credible solutions from hype and time adoption for ROI.

- Business Development: Spot which prospects are ready now versus too early.

- Investors and Bankers: Evaluate risk-return profiles, bridge FOAK funding gaps, and see when sectors cross from venture to infrastructure.

Overall, the transition isn’t one smooth curve. Some technologies are scaling now, others are years away, and many will face setbacks. That uncertainty is exactly why decision-makers need a structured way to track readiness.

The Sector Readiness Framework is Sightline’s answer: a data-driven, battle-tested lens for understanding commercialization.

👉 If you’re interested in learning how to apply Sightline’s Sector Readiness Framework to your strategy, innovation, or investment decisions, talk to our team.