.svg)

.png)

Stratos-pheric stakes in Direct Air Capture (DAC)

Direct Air Capture (DAC) has long been seen as way to make a big dent in global CO2 emissions, sucking CO2 out of the sky and storing it underground for thousands and thousands of years (if you want to hear a fantastic pod about this w/ yours truly, see here). But like most new tech, it doesn’t make sense to even put it in the game until it makes economic sense. And for a handful of oil producers, that seems to mean, use DAC for EOR.

Enhanced Oil Recovery (EOR) — injecting CO2 into depleted fields to extract the last volumes of oil — is well understood to be economically viable for producers, especially in areas like the Permian Basin, when oil prices are around $50-60/bbl. However, it becomes even more attractive when prices exceed $70/bbl. This was evident when Exxon acquired Denbury on July 12, 2023, with West Texas Intermediate (WTI) at $75/bbl. Exxon’s primary interest in Denbury was its extensive 1,000-mile CO2 pipeline network, natural CO2 fields, EOR assets, and access to storage sites.

But what do you do if you have production assets (i.e., older oil fields) ready for EOR, but you want to avoid the headache and cost of sourcing CO2, building pipelines, or (gasp!) paying to use someone else’s pipeline? You turn to DAC, of course. Okay maybe not ‘of course’, but this way you secure your own CO2 supply, on your own terms.

Oxy announced the acquisition of DAC tech provider Carbon Engineering on 16 August 2023, when WTI was $81/bbl. The press releases made the case for the environmental advantages and that it plans to deploy about a hundred DAC units, but didn’t specify exactly where — my guess would be on well pads.

This acquisition also re-started the marquee Stratos project (Sightline client-only case study here), which was initially slated for EOR. Then, companies like Amazon, Microsoft, and TD Securities stepped in, purchasing the majority of the credits from the 0.5MtCO2/yr project. Word is, the project is nearly complete and set to come online later this year.

This got us thinking: What’s going on with DAC? Well, using the Sightline platform, here's what you can tell.

1. 2025 will be the "prove it" year for DAC.

There are six (6) DAC projects currently under construction, but 1PointFive’s Stratos project (CO2 capture by Carbon Engineering / Oxy) is by far the largest, taking the entire DAC sector from 0.016MtCO2/yr to over 0.5MtCO2/yr. So it’s all eyes on Stratos.

This will not only be a test of whether DAC can work for EOR, but more broadly, it will also determine whether DAC can be a viable offset pathway. With the voluntary carbon markets demanding higher-quality removals and SBTi tightening standards for corporate net-zero claims, the pressure is on for DAC to scale. The long-awaited launch of Stratos could set a new benchmark and maybe even restore some investor confidence.

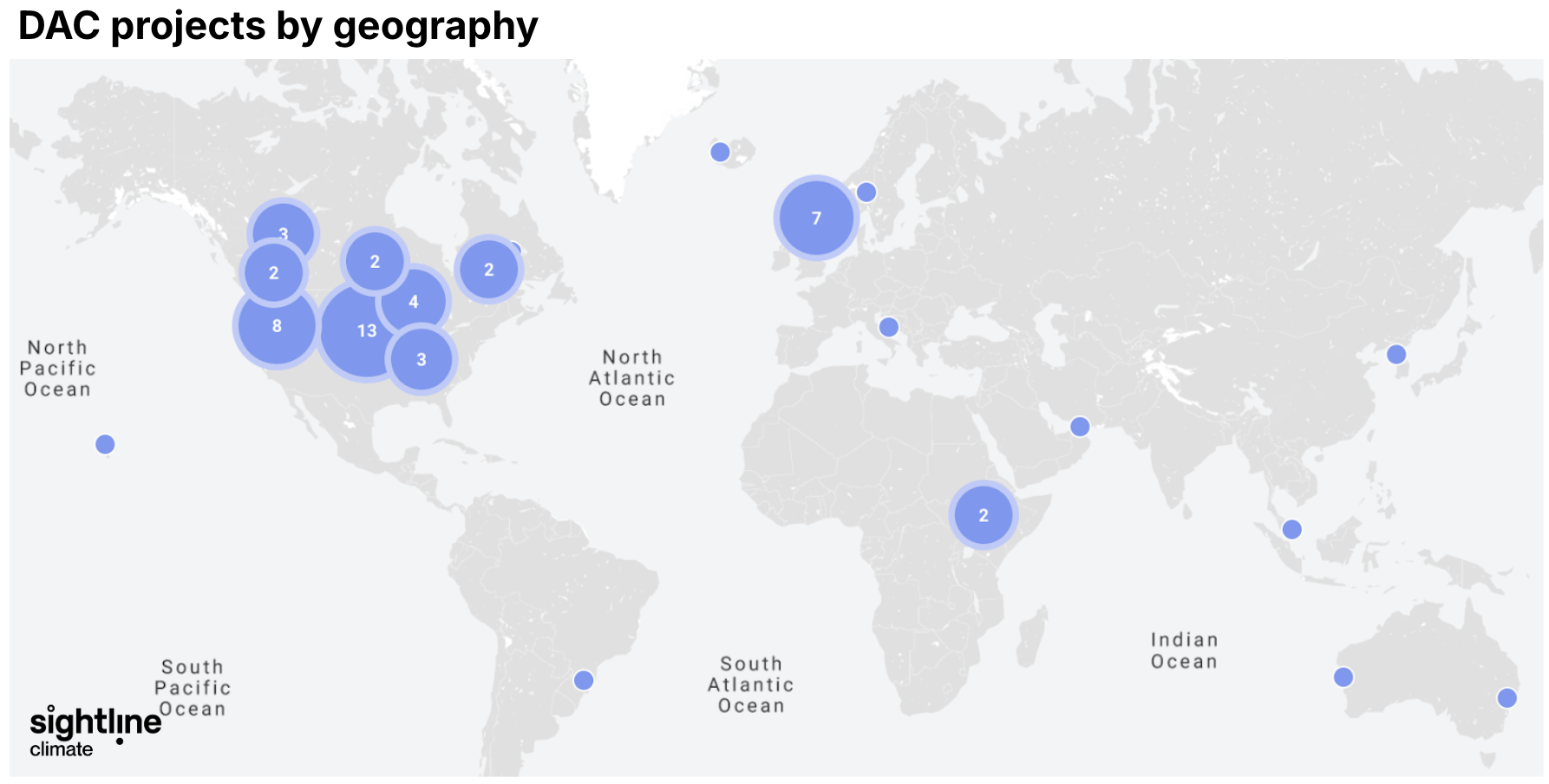

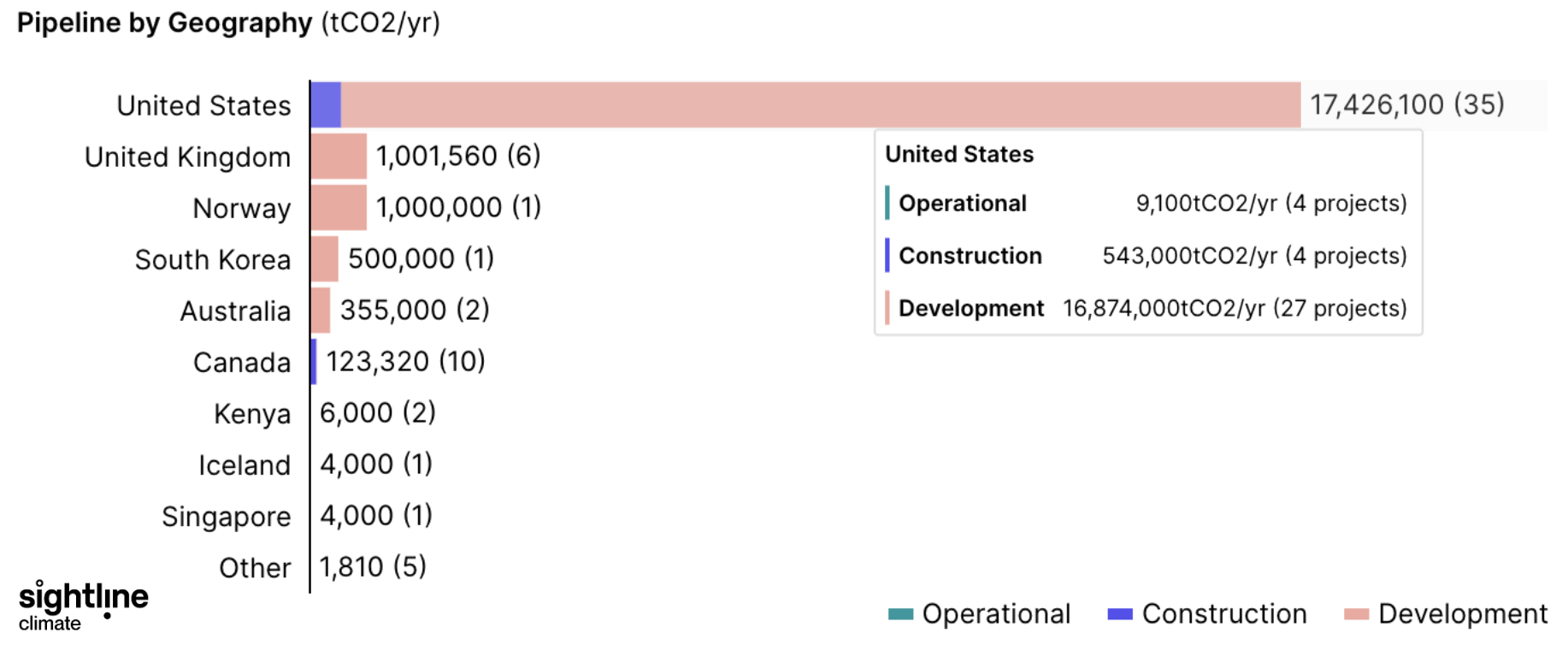

2. Location, location, location.

Most DAC capacity in development is in the US — by a mile. There are 35 projects in the US averaging about 0.5MtCO2/yr each, the bulk of which are in areas that could presumably be used for EOR, like Texas, Louisiana, and New Mexico. Of those 35 projects, 27 are in pre-construction development, and per our analysis, have geologic storage as the CO2 destination — but a combination of oil price (if it stays above $50/bbl) and 45Q tax credits could push this geologic storage into EOR territory.

3. Game of tons. Most projects are still hanging out in Lab-land. The chart below is what we call the “Race to Scale” — or, who is building the first large-scale commercial projects. Here, we’ve left out pre-construction development projects, and we’re just looking at what’s getting built. It’s pretty striking that of the companies supplying DAC, only two are really going big right now — Carbon Engineering / Oxy, and Los Angeles-based Equatic. Almost everyone else is still in the Lab or Pilot phases… waiting to see what happens with Stratos.

.png)