.svg)

.png)

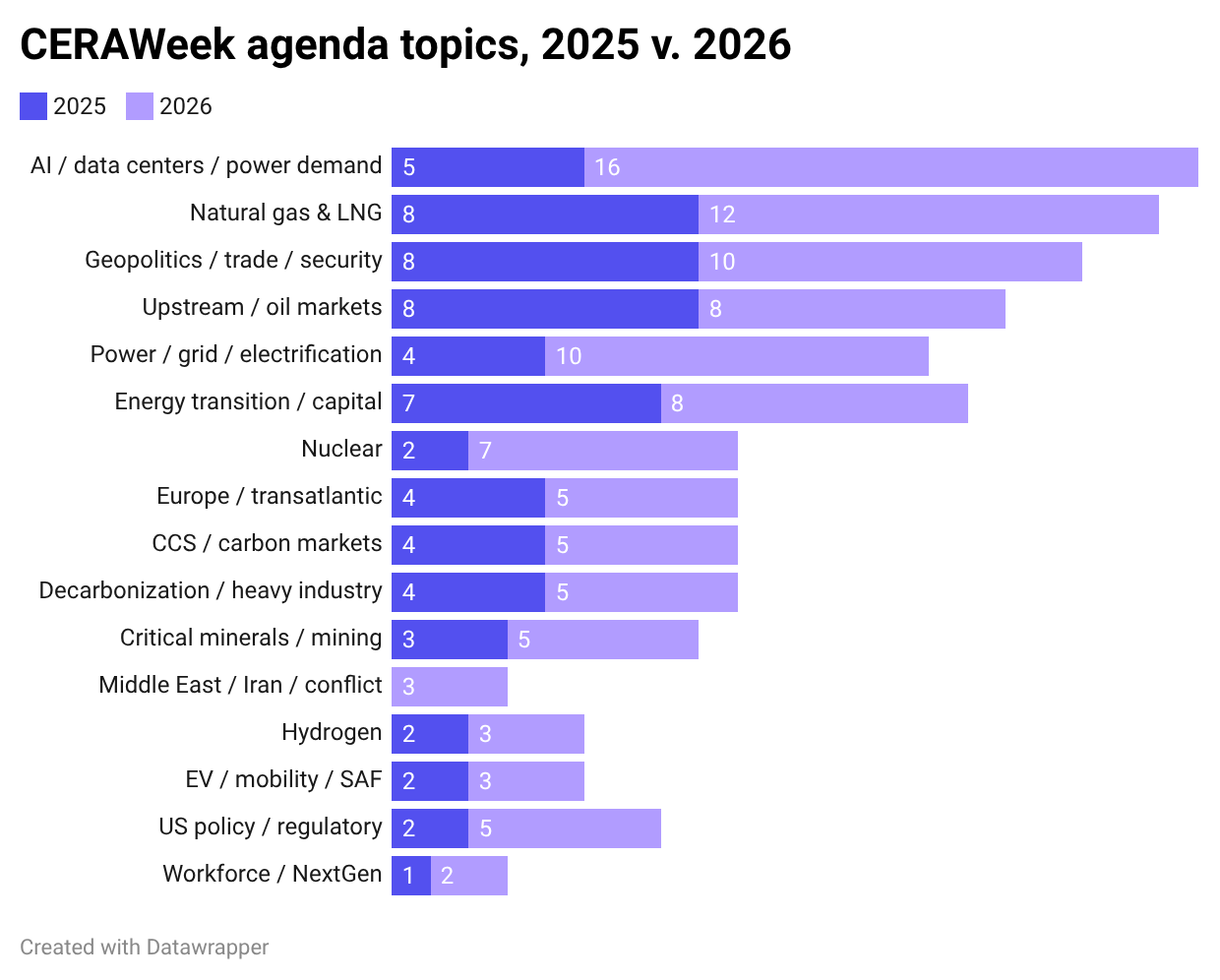

CERAWeek 2026: Disruption is the new normal

.png)

CERAWeek just made one thing clear: Houston, we have a queue problem.

This year, the “Superbowl of Energy” was set against the backdrop of a war in the Middle East, the continued race to power AI, and of course 4+-hour TSA lines at the Houston airports.

The main throughline: Disruption is increasingly the new normal. And you can see and feel it most clearly in the queues. People around the world waiting for fuel supply. Generation and data center projects stuck in years-long interconnection queues. TSA lines stretching all the way from the basement as the US works through yet another government shutdown.

Like last year, Secretary of Energy Chris Wright kicked off the week in a speech that used similar Energy Dominance rhetoric: “The world is energized by hydrocarbons. That’s a fact that guides our administration.” But there was more ground to cover this year. Wright had to toe the line between “America First” and trying to appease global concerns around the US’ uncertain moves and future with Venezuela and Iran. Then he had to shift to the other supercycle playing out, America’s place in the AI power arms race.

The speech was a sign of the times. Over in the Executive conference, behind-the-scenes discussions took on the impossible task of predicting short and long-term impacts of the Iran War. Meanwhile, at the Agora conference (CERAWeek’s innovation side event, now a main event in its own right), conversations centered on US power and data centers. Everyone jockeyed to get their low-carbon data center or speed-to-power play of choice in front of the hyperscalers, but the narrative has shifted from just pure speed to also energy affordability.

TLDR: CERAWeek laid bare that we’re in a sharp return to the New Joule Order, as Carlyle’s Jeff Currie and James Gutman have laid out. Energy security first, affordability second, environment (unfortunately) third. And all on an increasingly regional scale. But even if the energy world is no longer putting environment first, don’t call it a trilemma. Look at Pakistan’s saving $6.3bn this year by using solar instead of buying O&G at current elevated prices. Or the need for speed and off-grid data centers delivering the next battery boom, even in long-duration.

At a glance: Everything's bigger in Texas

- Big crowds: 11,000+ people at the 44th CERAWeek, more than the 10,000 last year. More than just energy, tech execs were everywhere this year. S&P Global introduced "The Bridge," a new venue specifically for energy-tech crossover conversations.

- Big names: A who's who of oil, gas, finance, tech, government, and innovation, plus a Nobel laureate.

- Oil & Gas: Chevron, Aramco, Exxon, Shell, TotalEnergies, Occidental, BP, ConocoPhillips, EQT

- Finance & Trading: Carlyle, Lazard, BlackRock, Mercuria, Trafigura, Glencore

- Government & Policy: US Secretaries of Energy (Chris Wright) and Interior (Doug Burgum), EPA Administrator Lee Zeldin, FERC Chair Laura Swett, National Energy Dominance Council Executive Director Jarrod Agen, ministers from Nigeria and the UAE. Venezuelan opposition leader and Nobel Peace Prize winner Maria Corina Machado was a last-minute addition.

- Tech, Data Centers & AI Infra: Microsoft, Google/Alphabet, NVIDIA, AWS, Meta, AMD, Meta, Dell, Applied Materials, AMD, Crusoe, Nscale

- Power & Utilities: NextEra, Constellation, AES, Vistra, Dominion, NRG Energy

- Equipment & Services: GE Vernova, Hitachi Energy, SLB, Baker Hughes

- Big stakes: A month into the US-Israel-Iran war. Strait of Hormuz nearly closed. Oil at ~$100/bbl. Gas up 30%+. Diesel over $5. The planned theme of "Convergence and Competition" was overtaken by security and affordability. The irony of the theme was that the world seemed to be getting more multipolar, rather than converging. The focus on domestic energy security also gave rise to conversations about adaptation and geoengineering.

- Big announcements: TotalEnergies' $1bn wind-to-gas swap with DOI. NVIDIA's "Flexible AI Factory" partnership with six major utilities. Microsoft + NVIDIA AI-for-nuclear collaboration. EPA E15 summer waiver. EIA pilot surveys to track data center energy use in Virginia, Washington, and Texas.

Top five takeaways

1. Geopolitics makes the energy map multipolar

The Middle East crisis is playing out in macro game theories about who has buffers…and who doesn’t. China is the most exposed by volume but has the most options (significant renewables and coal capacity, pipeline imports from Russia). South Korea and Japan have deep LNG storage and cargo-swapping agreements. Taiwan sources ~30% of its gas through routes now under pressure and India is likely to face rationing. Vietnam and Thailand are caught between a decline in domestic gas production as they have tried to develop their own renewables capacity. Meanwhile, rapid solar adoption has helped cushion the impact in Pakistan.

Even if the physical impacts of this energy market disruption are short-term (which seems less and less likely given LNG infra damage), the mental impacts will remain long-term. Once disruption becomes the new normal, countries will build their energy strategies for that.

Overheard

"What makes hydrocarbons so great is they're portable and storable, that also makes them dangerous when you're dependent on a strait." - Jeff Currie, Carlyle

2. Power and molecules continue to converge as AI creates opportunities

Everyone is trying to get a share of the multi-billion hyperscaler capex pie. The renewables developers and O&G majors alike are getting creative with turning existing assets into something useful for hyperscalers. Whether it’s powered land sites previously built for hydrogen (read: Google, Intersect deal) or combining CO2 pipelines and gas infra into low-carbon data center-ready assets (read: Gas data center moment).

Tech companies are already behaving like energy companies: Google has secured over 1GW in demand response capacity, while NVIDIA is designing grid-aware chip architectures. This convergence is driving massive demand for grid software, storage, flexible generation, and efficiency solutions. (We covered the week’s flexibility announcements in Powerstack: EPRI's Flex MOSAIC framework, NVIDIA/Emerald AI's flexible AI factory partnerships with six major utilities, and Octopus Energy's acquisition of US demand-side platform Uplight).

And it cuts both ways. Energy companies are becoming power providers first. Chevron already has 5GW of off-grid power assets to run remote LNG + refining operations. Williams is building BTM generation so customers sign one PPA and get a turnkey solution.

3. Gas is America's self-proclaimed superpower

Wright's keynote set the tone for the week: the administration sees natural gas as the load-bearing wall of US energy policy, the way to win AI dominance, and re-energize domestic manufacturing.

It was a lot of chest-thumping onstage, but behind the scenes, people were a lot more pragmatic. Sure, gas for security and affordability, but its path isn’t immediately the smoothest. McKinsey estimates an additional 4.1bn cubic feet per day (BCFD) of gas demand for power generation in the US and Canada by 2030. But procuring new gas turbines has a 6-7 year lead time and has tripled in cost over a few years. There’s even more talk of congestion issues with gas pipelines, just like with interconnection queues.

Of course, in the main conference, most talks referred to unabated gas. Over in the Agora, a few sessions covered gas with CCS, which faces its own supply chain disruptions and added complexity because of CO2 transport and storage. DAC companies like Spiritus and Yama talked about their new strategy both pivoting to gas applications. Throughout, CO2 utilization for EOR was louder than storage.

Overheard

"America’s superpower is natural gas. Natural gas is the key for the US to lead in AI and build back energy intensive manufacturing." - Chris Wright, Secretary of Energy

“Even with the slowdown of demand, where does supply come from?” - Geoff Houlton, Senior Vice President, Oxy

4. Next-gen clean firm power and critical minerals had the strongest showing in years

The administration came in swinging on nuclear. Wright announced an ambition for three next-gen reactors "running and generating heat" by July 4 (early safety system runs, not full commissioning), with 11 total in the queue. Fusion made its most credible showing yet — TAE Technologies ($1.4bn raised, going public via reverse merger) targeting a first 50MW plant by ~2031-32, Type One Energy designing a 400MW plant with TVA for mid-2030s.

And geothermal may have stolen the show: Project InnerSpace hosted a dedicated Geothermal House for the first time, launching a standardized resource classification framework (GRMS) with the Society of Petroleum Engineers and an XPRIZE collaboration targeting surface-plant supply chain breakthroughs.

Behind all of it sits a critical minerals supply chain that still runs through China. A main topic of conversation was de-risking and funding domestic solutions, one of the few areas with genuine bipartisan consensus. Federal policy is doing the heavy lifting: $225m DOE grants, 48C credits, expedited permitting. Arkansas is building a full lithium ecosystem.

Overheard

"If we want to win in AI, we have to build a lot of power. Natural gas now, as fast as you can, and nuclear technology as soon as we can get it moving." - Chris Wright, Secretary of Energy

5. The devil's in the permitting, labor details

Across panels, from O&G, to nuclear, to transmission and data centers, permitting and labor constraints came up. ConocoPhillips said its Willow project in Alaska took four years to build but five years to permit. On the nuclear side, BlueEnergy and Crusoe nuclear-powered AI data center project in Texas is using low-risk reactor technology for project financeability and faster permitting. The US and UK are developing fusion-specific permitting frameworks, separate from fission, with timelines of roughly two years versus decades. In transmission and data centers, every infrastructure conversation assumes a workforce that doesn't exist. Google recently partnered with the electrical training ALLIANCE (etA) to train 100,000 existing electrical workers and 30,000 new apprentices in the US. Suddenly being an electrician, a plumber, or a welder is cool, but the training pipeline is years behind demand.

Overheard

"You can't build infrastructure if it takes 5 years to permit it." - Helen Currie, Chief Economist, ConocoPhillips

“I keep telling everyone, go get your certifications, you are about to make a lot of money.” - Amanda Peterson, Global Head of Data Center Energy, Google

.jpg)

.jpg)

.png)