.svg)

.png)

Data center outlook: half of 2026 pipeline may not materialize

Announced capacity for 2026 suggests another year of explosive growth for data centers. But our outlook on the market suggests that 30–50% of that pipeline is unlikely to come online before the end of the year.

With so much information flooding every sector, Sightline Climate is launching Outlooks, a quarterly update designed to give a clear forward-looking picture of the market, pull out meaningful signals and trends from the market.

Outlooks combine the real-time data ingestion from our AI engine with analyst context to get you rapidly up to speed on two questions:

- What’s the state of the market today?

- What should you be planning around this quarter?

The Data Center Outlook is the first in this new series, precisely because of all the hype around hyperscaler build out and the power bottleneck it’s creating. You can download a public version here.

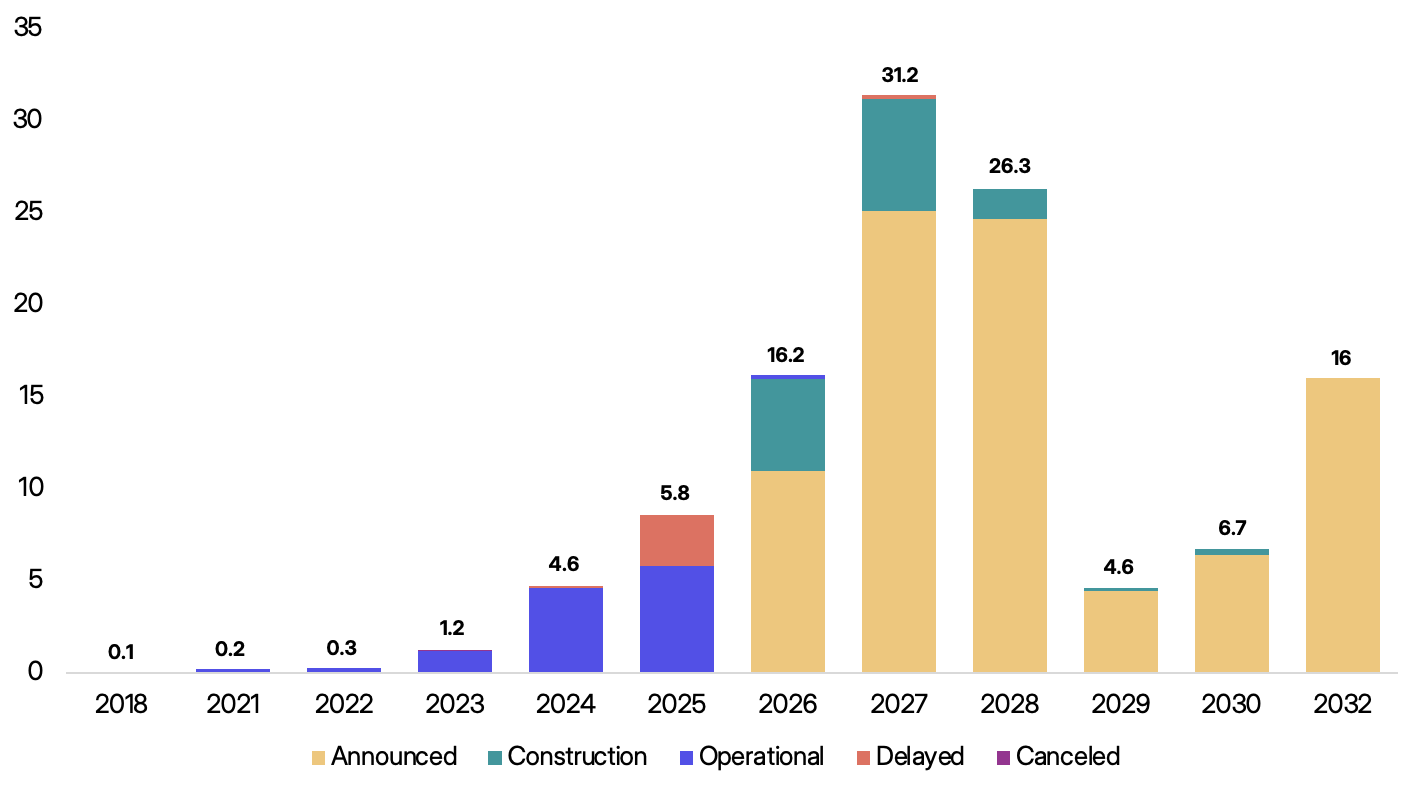

We’re tracking 190GW across 777 large data centers and AI factories (>50MW) announced since 2024. At least 16GW of capacity is slated to come online in 2026 across roughly 140 projects. Yet only about 5GW is currently under construction. Around 11GW remains in the announced stage with no visible construction progress, despite typical build timelines of 12–18 months.

Projected delivery dates are getting harder to trust. In 2025, 26% of expected capacity slipped, and another 10% of projects pushed back their commercial operation dates without much notice.

Given that track record, it wouldn’t be surprising if 30–50% of the capacity slated for 2026 ends up delayed.

The Outlook Underscores the Power Bottleneck

Hyperscalers are increasingly giving up on the grid for AI training capacity.

While grid-connected remains the most common powering model by project count, sites with their own power sources on-site and hybrid approaches account for a disproportionate share of gigascale capacity. New Era Energy & Digital's 7GW project in New Mexico, for instance, is large enough to justify its own generation.

On-site and hybrid approaches remain niche in terms of project count, together accounting for less than 10% of total projects. However, they represent nearly half of announced capacity, punching well above their weight when measured in MW. This imbalance is driven by a small number of gigascale, grid-independent campuses.

At the same time, nearly half of projects haven’t disclosed a power strategy at all.

Some hyperscalers are even going further to secure power closer to the source. Google’s acquisition of Intersect Power’s 10.8GW pipeline and Amazon’s direct investments in solar and storage signal a new willingness by hyperscalers to secure power at the project or portfolio level, rather than the typical PPA approach, in order to accelerate deployment.

How Sightline Climate Clients Use the Data Center Outlook

The Data Center Outlook is designed to support planning and investment decisions.

Utilities and grid operators

Need to anticipate large-load demand, structure interconnection frameworks, and assess where flexibility or on-site generation will become standard.

Hyperscalers and developers

Must distinguish speculative pipeline from executable capacity and evaluate trade-offs between grid-connected, hybrid, and on-site models.

Infrastructure investors and lenders

Require clarity on which projects have secured permits, power, capital, and tenants — and which remain early-stage announcements.

Power providers and equipment manufacturers

Use Outlooks to understand where demand for backup generation, BESS, and bridge-to-grid solutions is accelerating.

Methodology

The Data Center Outlook is built on Sightline Climate’s live project database, tracking 190GW across 777 data center projects announced since 2024.

Data is continuously updated and normalized for comparability. Each quarterly Outlook synthesizes changes in deployment, capital flows, regional concentration, and policy shifts, underpinned by the categories in our Readiness Curve.

Download the Report

We’re sharing a public version of the Data Center Outlook with key charts and topline findings. You can download it here.

For the full dataset, project-level tracking, and quarterly updates, Sightline Climate clients can access the complete report within the platform.

If there's one thing you read every quarter, it should be this. Carbon is already out. Clean firm is due in early March with Fuels following in mid-March.

Watch the Data Center Outlook webinar below, featuring Vlad Oujegov, President of Western Canada Data Centre Alliance, Ben Alingh, CEO and Co-Founder of Monarch Energy, and Thomas Schuldt, BD and strategy at DG Matrix.

.jpg)

.jpg)

.png)

.png)