.svg)

.png)

Analyst Take

Texas gains ground and wins state control over carbon storage

Author:

Paola Saenz

Updated:

November 24, 2025

So what

Texas’ new Class VI primacy puts nearly a quarter of all US CO₂ storage applications under a faster, more predictable state-run permitting process, potentially cutting review timelines by more than half. This shift accelerates CCS and DAC deployment in the state, where strong geology, dense industry, and existing infrastructure already give Texas an advantage. With federal financing pulling back, Texas’ regulatory certainty makes it one of the most important and investable jurisdictions for carbon storage in the US.

What happened

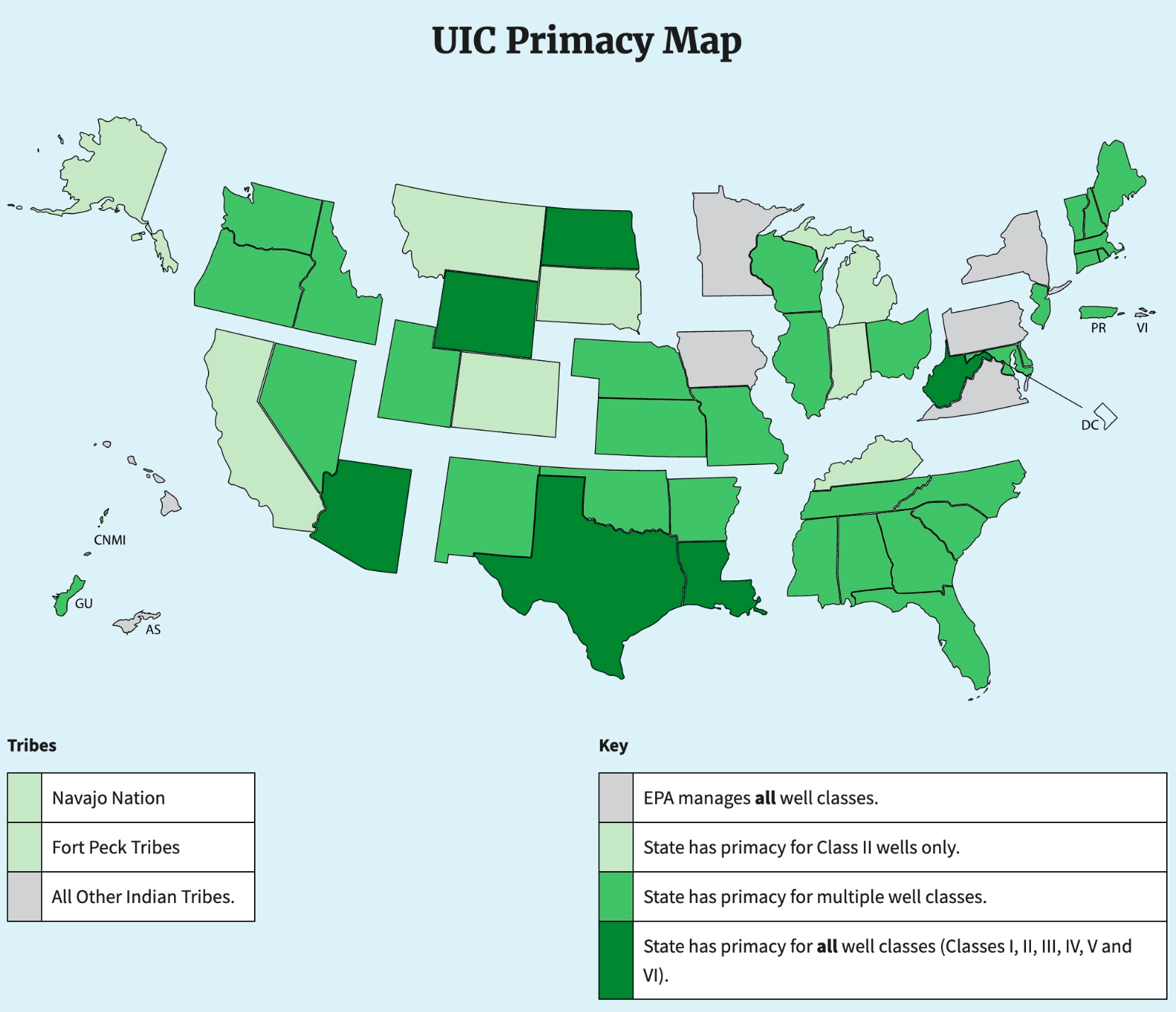

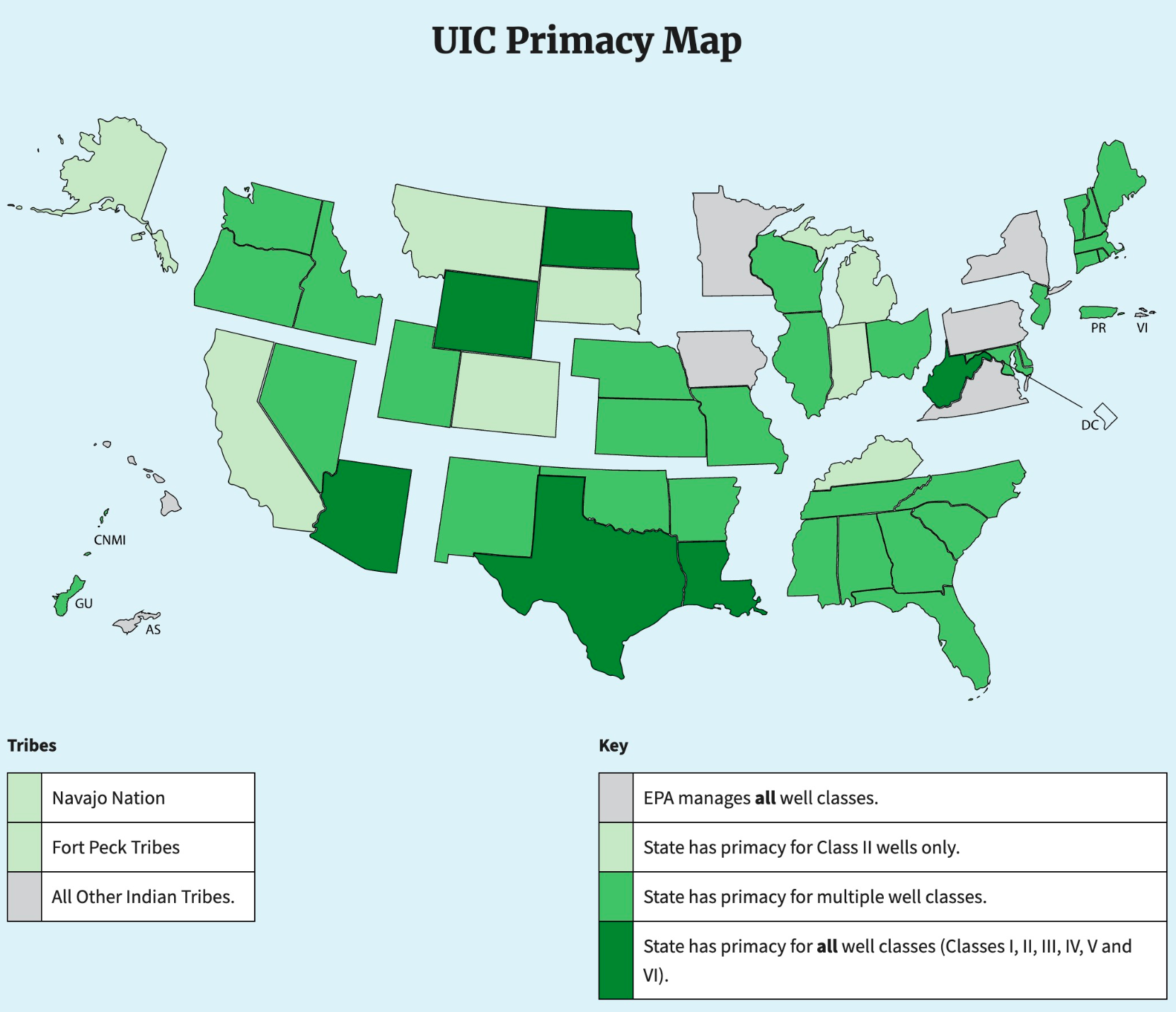

- On November 12, the EPA finalized Texas’ Class VI primacy, granting the Railroad Commission of Texas (RRC) full authority to permit, enforce, and oversee CO₂ geologic sequestration wells. Texas became the 6th state with Class VI primacy, joining North Dakota, Wyoming, Louisiana, West Virginia, and Arizona.

Source: EPA

Why it matters

- Everything is bigger in Texas, including CCS. Texas hosts some of the largest CCS and CDR projects in the country, from legacy infrastructure like Petra Nova to next-generation DAC projects like Stratos, the world’s biggest liquid DAC facility under construction. With 61 Class VI wells under review across 18 projects, Texas alone represents nearly one-quarter of the entire US Class VI pipeline, meaning primacy could immediately affect the pace of national deployment.

- Primacy could shorten permitting timeline up to 60%. Class VI well reviews under the EPA frequently take between 24–30 months, Exxon’s and Oxy’s recently approved permits in Texas took 18 months and 30 months respectively. State-run systems have performed much faster with North Dakota’s shortest permit approval in 8 months. Shorter and more predictable timelines can create certainty for developers and investors and accelerate path-to-operation for dozens of projects in Texas.

- A win in an era of regulatory and financing uncertainty. With DOE loans cancelled for several CCS and DAC projects—including major DAC hubs in Texas and Louisiana—the sector is facing heightened financial pressure and a shift toward higher-cost private capital. For CDR projects, public financing can keep removal costs near $171/tCO₂, while FOAK project financed with private lending rates can see those costs rise to around $322/tCO₂. Texas’ primacy, however, could help rebalance project economics, as faster, more predictable permitting could shorten development timelines and lower total project costs.

What’s next

- The first permits likely to be approved are Orchard Storage Company, Milestone Carbon Midland CCS Hub and Pineywoods CCS. Under primacy, these projects could receive decisions by the beginning of next year.

- California’s absence from the primacy landscape is increasingly conspicuous. While other states like Alaska, Mississippi, Nebraska, Utah, Alabama, New Mexico, and Oklahoma have already entered Phase 1 pre-application discussions with the EPA, California has yet to pursue primacy despite having one of the largest CCS/DAC project pipelines in the country. This gap may increasingly push developers and investors to prioritize states offering faster, clearer regulatory timelines.

Get full access to our research

Resources

.jpg)

.jpg)

.png)

.png)