.svg)

.png)

🌍 Your 2026 prediction bets

.png)

Every year, we ask you to place your bets on what comes next in climate and energy: where capital flows, which companies scale, what technologies actually deploy, and which parts of the ecosystem don’t survive the next cycle. Then we track the tape at the end of the year to see which calls paid out and which ones missed.

This year, nearly 500 of you weighed in on our 2026 Predictions Survey, setting the market odds on the next phase of the energy transition. It’s our crowd-sourced prediction market — no contracts, but lots of conviction.

Below, you’ll find the aggregate results, with all the crowd favorites and the long shots, for everything from investment totals and geography to grid assets and climate hazards.

We didn’t stop there. We then stress-tested those bets with a smaller group of investors, operators, and policy insiders. We asked the experts the same questions and got their takes on what the market is getting right, what it’s mispricing, and where consensus could break. And bonus: the expert reflections on the year and what’s ahead.

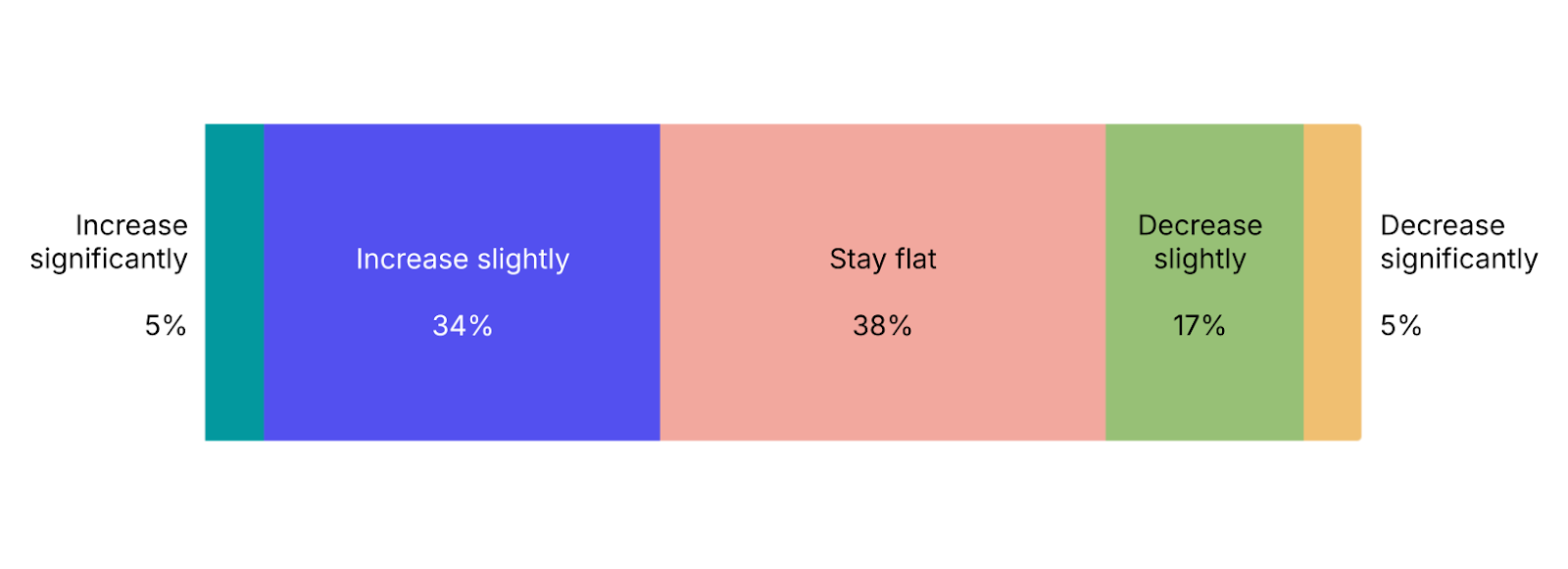

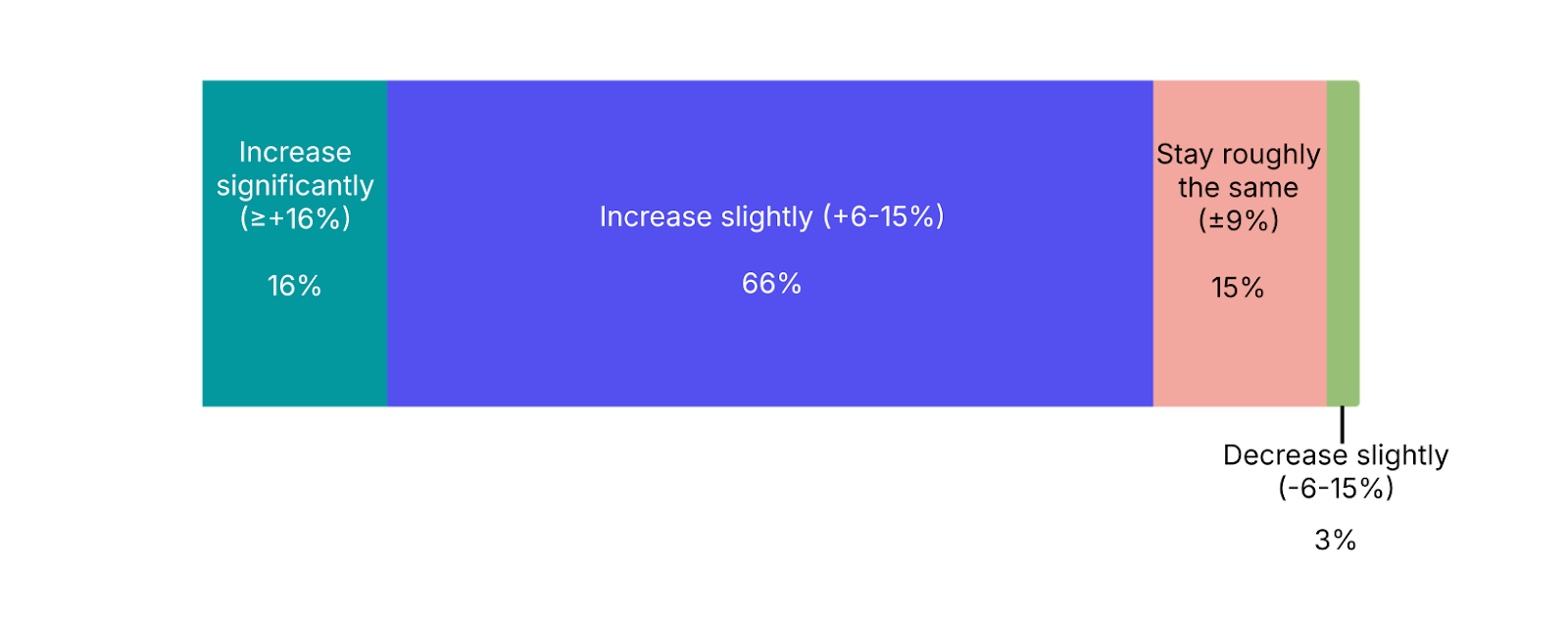

1. Will climate tech venture / growth funding in 2026 …

Results: Most of you expect funding to stay flat or increase slightly. That’s directionally in line with 2025 investment, when climate tech venture and growth was up 8% from 2024, clocking in at $40.5bn for the year.

Expert takes:

“Increase. Soooo much money has been raised globally for climate. That's got to go somewhere.” - Andrew Beebe, Managing Director, Obvious Ventures

“Funding will increase, but concentrate. Capital will continue moving toward companies that have crossed into repeatable deployment and can support layered capital stacks. Growth will favor teams that plan for durability from Series B onward.” - Caie Kelley, Partner, Lowercarbon

“Climate tech venture capital and growth funding in 2026 is likely to strengthen in 2026, in specific areas -- particularly those enabling the rapid deployment of critical energy infrastructure. Platforms leveraging vertical AI that help capital move faster will stand out. In a market defined by rising demand and tight timelines, the companies that attracted funding will be those positioned to execute at speed.” - Alfred Johnson, CEO, Crux

“Venture and growth funding will increase in 2026, benefiting from improving macro conditions despite lingering sector headwinds. This growth will be fueled by the Fed's ongoing rate cuts and more frequent early-stage company exits, both injecting capital back into the sector. After a two-to-three-year period that eliminated companies struggling with funding and commercialization, the surviving firms are poised to thrive and secure large investment rounds in 2026.” - James Frith, Principal, Volta

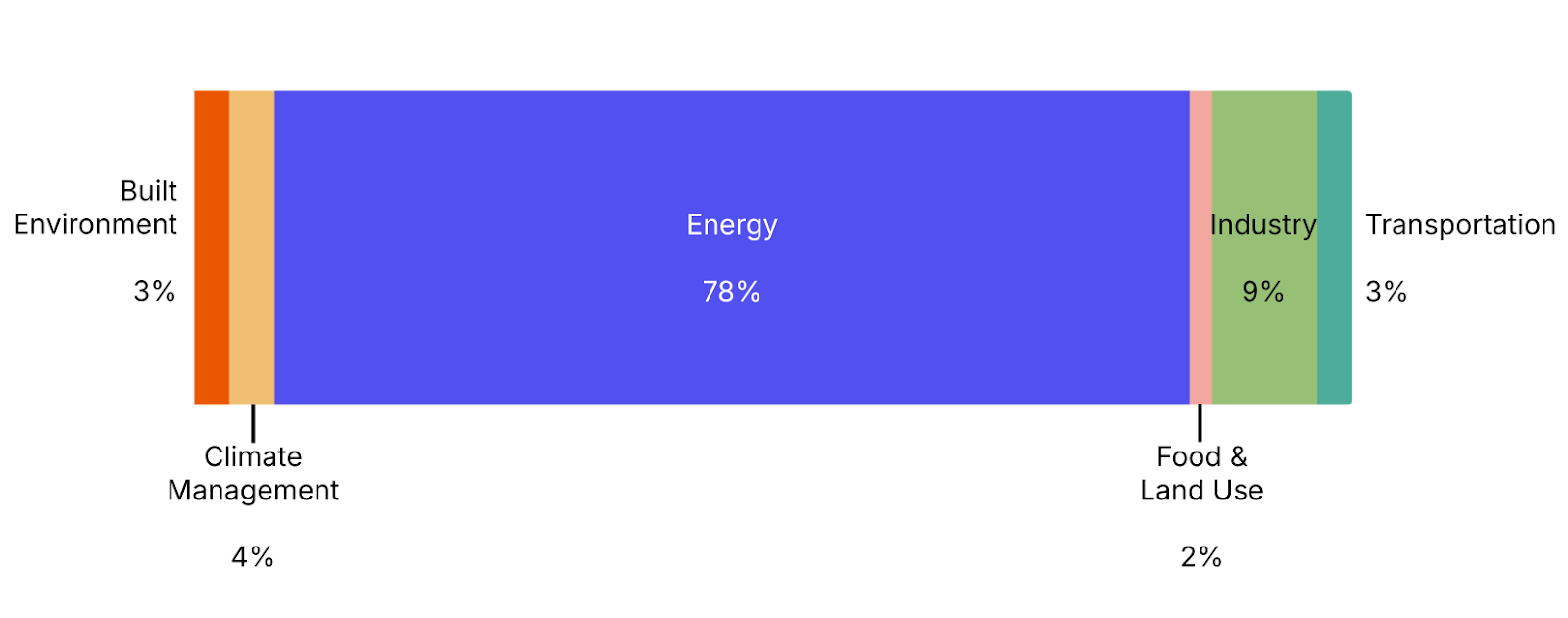

2. Which sector will receive the most investment?

Results: No surprise, Energy captured 78% of responses, an overwhelming consensus. Investment attention continues to consolidate around power generation, storage, and grid infrastructure as power demand rises from AI and electrification.

Expert takes:

“Energy, as the data center energy puzzle will pull forward innovation from demand flexibility and energy storage to geothermal and nuclear.” - Dawn Lippert, Founder & CEO, Elemental Impact

“Energy given the AI story, lots left there.” - Jeff Johnson, General Partner & Head of Energy & Resilience, B Capital

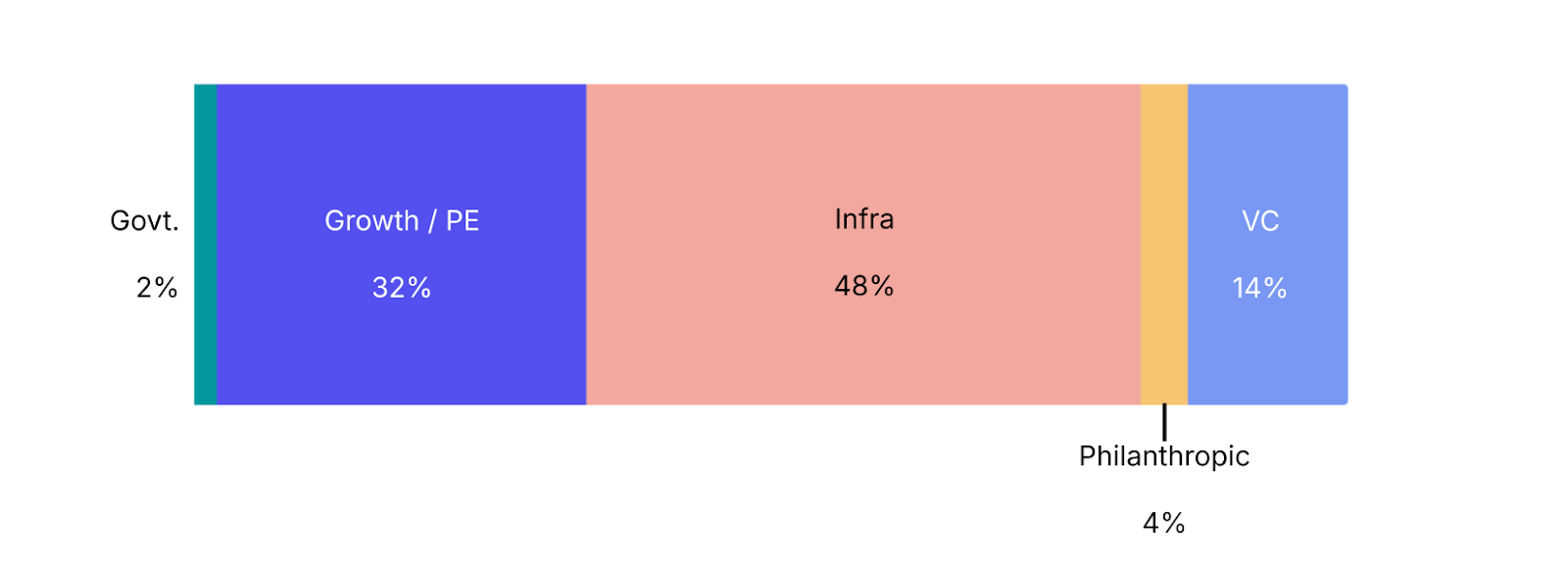

3. Which segment of the Climate Capital Stack will see the biggest growth?

Results: The mature layers of the stack got your vote. Infrastructure leads, followed by Growth and Private Equity. There’s a lot of confidence in the mature renewable-focused private capital.

Expert takes:

“Infrastructure capital. As deep tech companies mature, they increasingly resemble long-lived assets with contracted revenues. That naturally pulls in infrastructure investors, government programs, and hybrid vehicles alongside traditional equity.” - Caie Kelley

“I think philanthropy is ready for a big moment in the sun (the sun here being the climate capital stack). The shakeup of 2025 has shown that 1) innovation and markets have to deliver even more of the climate solutions we need with policy pulling less weight, and 2) the cracks in the capital stack have become even deeper with the government rollbacks, meaning that more good companies and important solutions will fail without intervention. And there are lots of new avenues for philanthropy to be highly catalytic and make a huge impact.” - Dawn Lippert

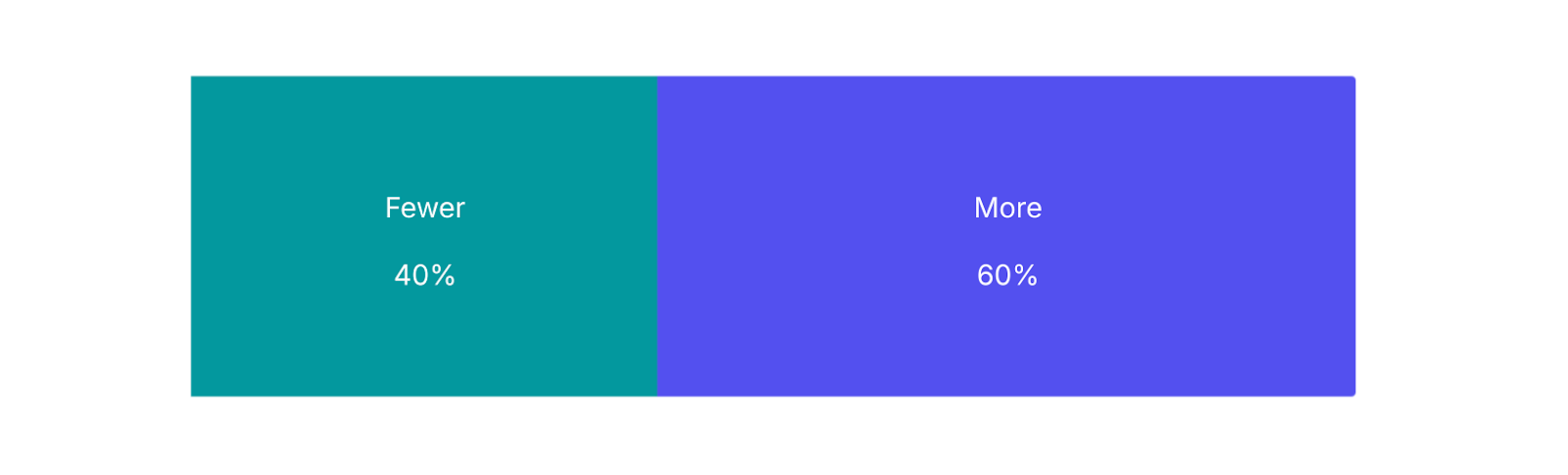

4. More or fewer exits in 2026?

Results: It’s a hungry market, and you’re betting on more exits ahead, even if the bar stays low. Exits fell 5% in 2025, driven by a dip in acquisitions, which still made up 89% of all exits in today’s buyer’s market.

Expert takes:

“More exits. The market has started opening up and I don’t think Trump will pull off another “tariffs”-like initiative. The pipeline is robust and investors want to see money back.” -Shira Eting, Partner, Vintage Investment Partners

“Far more exits, as the electricity supercycle expands and companies already at scale monetize.” - Jigar Shah, Co-Managing Partner, Multiplier

“More. Blockbuster IPOs like SpaceX and Databricks will open the IPO window wide for late stage companies performing well, and more companies that have exhausted their last bridge round will be picked up by strategic buyers in 2026.” -Dawn Lippert

“I expect we will see a significant increase in exit activity in 2026. This trend is fueled by the improving macroeconomic environment and the continued growth and rising revenue generation of companies that successfully navigated the last two to three years, but be prepared for some high profile failures as well.” - James Frith

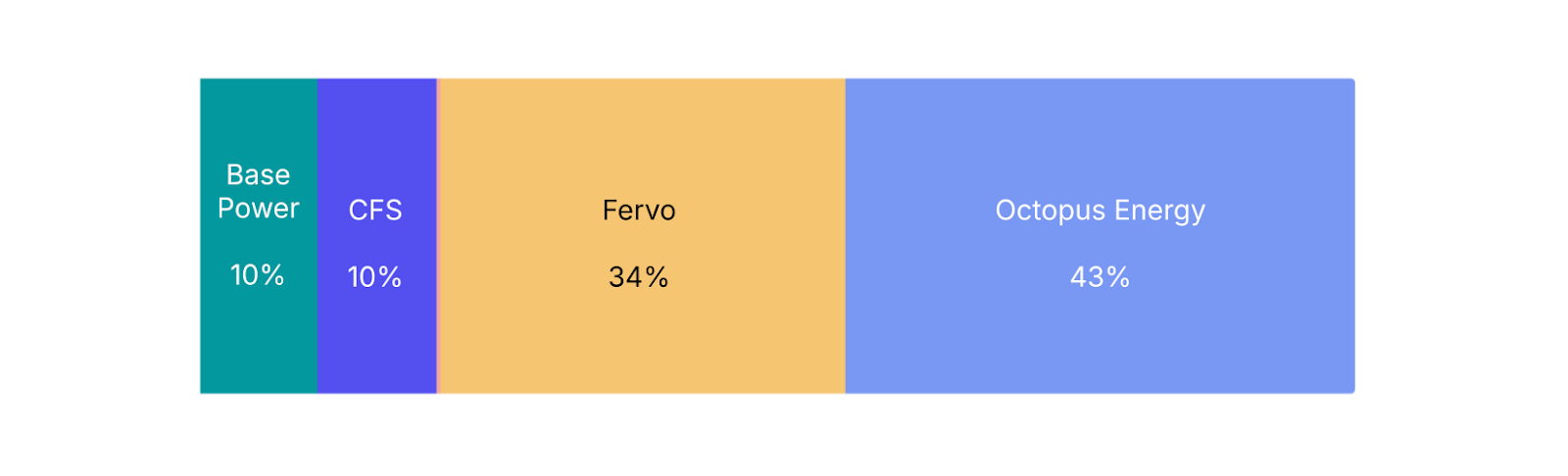

5. Most likely to IPO in 2026?

Results: Lots of bets on Fervo and Octopus Energy (although we did run this survey before Octopus spun out Kraken). Both companies have scale, operating assets, and revenue visibility. And some write-ins? “Radiant.” “Somebody in India.” “Some AI company.” “Nobody.”

Expert takes:

“Holtec, Fervo, over 20 more through SPACs.” - Jigar Shah

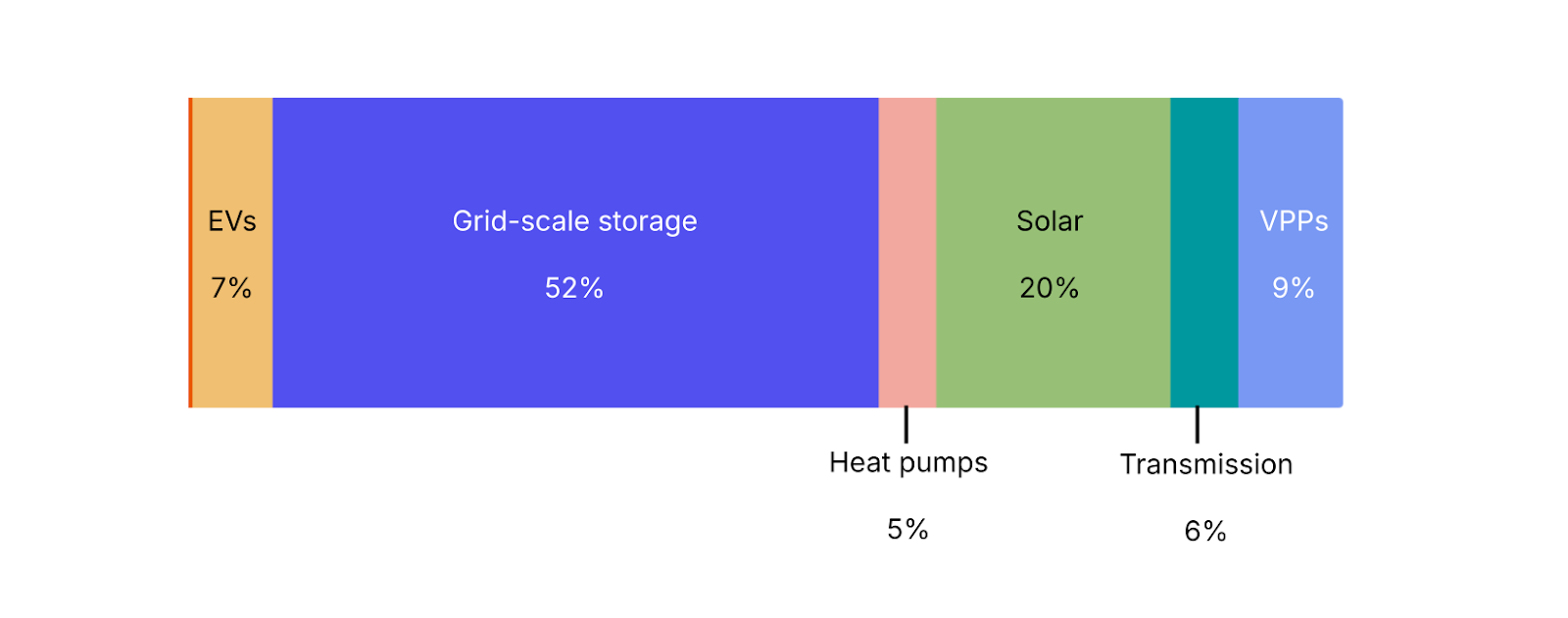

6. Biggest new deployment record?

Results: Grid-scale storage took the majority vote. Storage continues to move from a complementary technology to core infrastructure. Deployment expectations reflect bankability, supply chain maturity, and immediate grid need.

Expert takes:

“The newest important trend will be broader deployment of virtual power plants based on larger aggregation of vehicle to grid power. 2026 will be the first year in history where the majority of new EVs sold will provide bi-directional charging and energy transfer. As the revolution in AI and the increased number of data centers increases power demand from the world, utilities, virtual power plants will prove to be the lowest cost most personal solution for utilities.” - Steve Westly, Founder & Managing Partner, The Westly Group

“2025 was a breakout year for energy storage and we expect that to continue in 2026, likely setting new deployment records. Our data shows that in 2025 utility-scale battery installations are projected to reach 18.3 GW (a 78% increase over 2024), making storage the fastest-growing segment of the clean energy market. That growth is being driven by market economics: declining costs, rising power demand, and the need for dispatchable capacity as solar penetration increases. Storage is becoming a core component of grid infrastructure.” - Alfred Johnson

“Small, flexible thermal units such as RICE, aeroderivatives, and small turbines will see a massive increase in deployments over the next 24 months. Relatively inflexible units like fuel cells will also see a surge in deployments. There are four drivers: data centers cannot get online as quickly as they’d like to deploy new chips via utility power alone. Whether these units are operating as a microgrid or bolstering a utility connection as backup or peaking, manufacturing slots for these smaller, more flexible units are largely sold out until late 2028. Second, grid stability can benefit from smaller units. Utilities are deploying smaller units in a variety of jurisdictions, integrated into transmission corridors. So called “Texas-10s” fall within this category. Third, microgrids for oil and gas, as well as processing, continue to deploy these smaller units as they expand drilling to areas beyond the reach of the current grid. Fourth, data centers and other large industrial loads are being challenged in several jurisdictions to display flexibility. One way to do that is to ramp down loads. The other is to install flexible, on-site generation to take load off of utility grids. Note that many of these installations are paired with BESS to achieve reliability and load following capacity.” - Adam Mirick, Senior Energy Advisor, Prometheus Hyperscale

“Solar will have another breakout year. I know it’s probably storage, but despite FEOC requirements. And despite the PTC/ITC construction start or placed-in-service deadline — or because of them! — I bet record PV capacity gets built in 2026 as it trumps other technologies on cost and scalability.” - Mark Taylor, Co-Founder & CPO, Sightline Climate

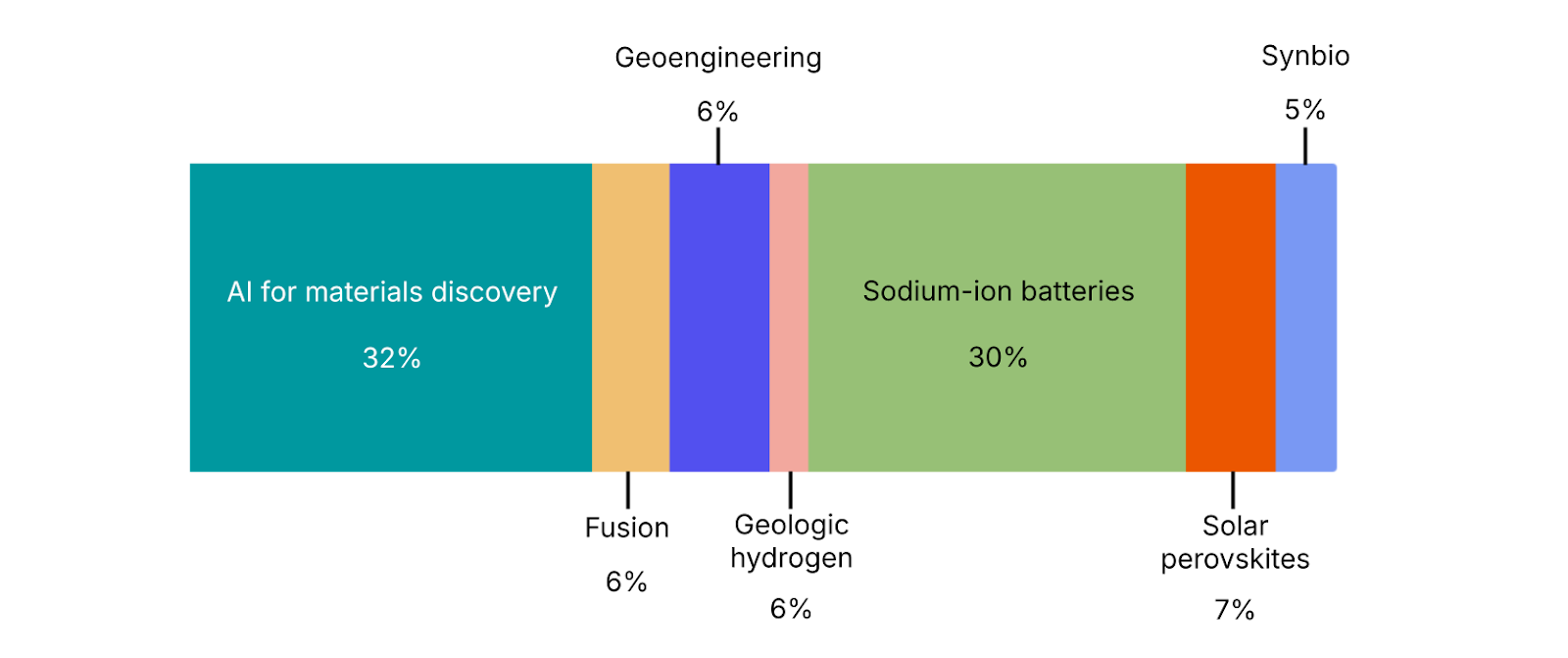

7. Frontier tech that will break through?

Results: Is this the year for AI for materials discovery or sodium-ion batteries? Respondents expect progress where tools shorten development timelines or reduce cost in existing systems. Some write-ins included: thermal storage, variable compute load, geothermal, AI for critical mineral recovery and grid optimization, and non-lithium-ion, non-sodium-ion storage.

Expert takes:

“AI for material discovery. When in doubt, bet on the models getting better and the resulting innovation. And this is a good thing: secure access to critical materials underpins US innovation, economic strength, and national security.” - Dawn Lippert

“Sodium ion batteries. The capacity exists for this in China already, it’s just not cost-competitive against LFP. LFP cell prices however, have been going up, giving sodium a chance. Solid state batteries, also, driven by continued growth in EVs and growing high-performance needs like drones and EVTOLs.” - Sharon Chen and Roger Zhang, Co-founders, Persimmon Systems

“We will see real progress on sub-50 MW nuclear reactors.” - Jigar Shah

“I believe the most interesting sector in the energy space is long duration energy storage. My view is that the ultimate winner will have minimal mined components, non-toxic solution capable of operating in a wide range of ambient temperatures without thermal runaway risk. People are focused on sodium-ion, solid state silver, and zinc bromide at present. These may win in the near term, but long term, I think we need to achieve materially lower cost than lithium cobalt, and this lilely means non-mined or very common inputs. The use of materials that aren’t hard or costly, in both environmental and human terms, will be a material win.” - Adam Mirick

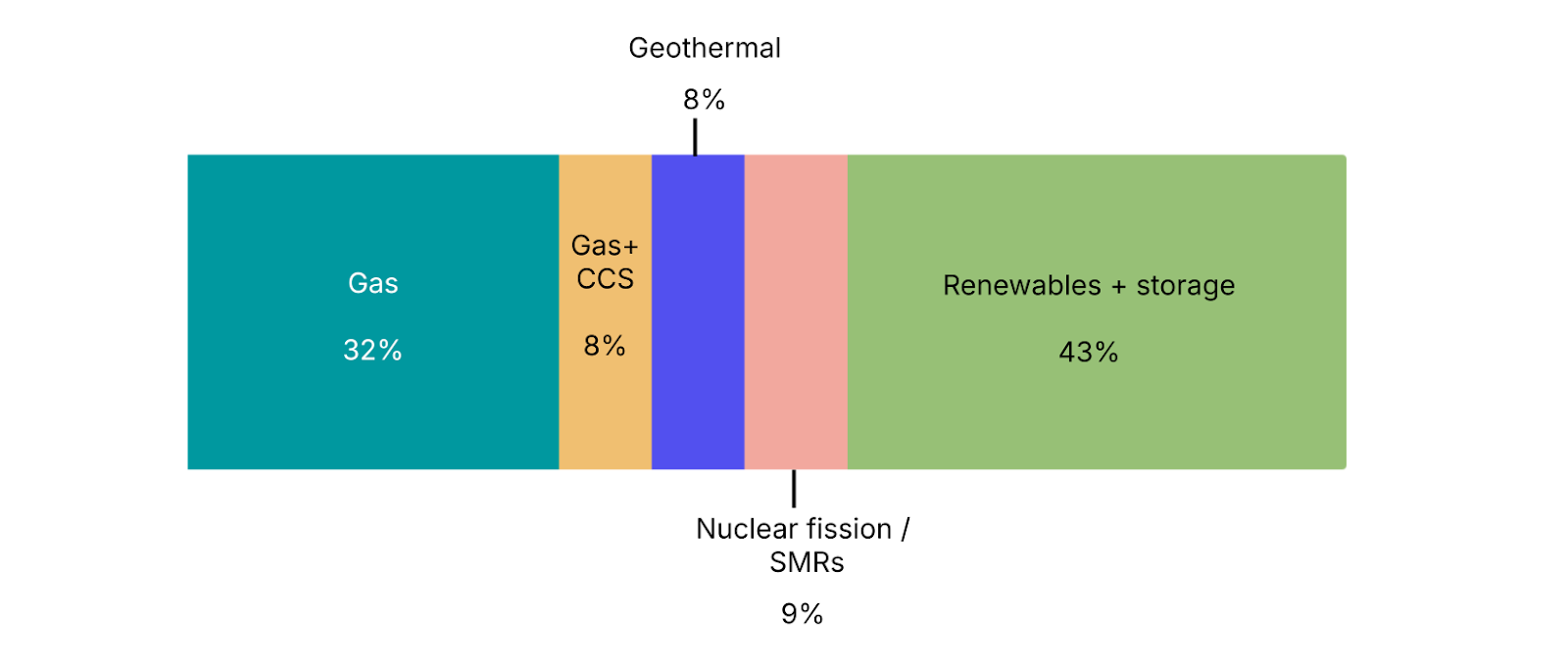

8. Fastest-growing power source for data centers?

Results: Gas remains a significant option, but renewables and storage is still the frontrunner.

Expert takes:

“Solar + BESS + Gas (turbines, recips) micro-grids. Hybrid stack that optimizes for uptime and time-to-power.” - Shanu Mathew, Investor

“I think grid connections WITH very large backup generation or storage systems to cut hours of peak load will be what we'll actually see come online this year. Serve the grid and skip the queue.” - Julia Attwood, Research Director, Sightline Climate

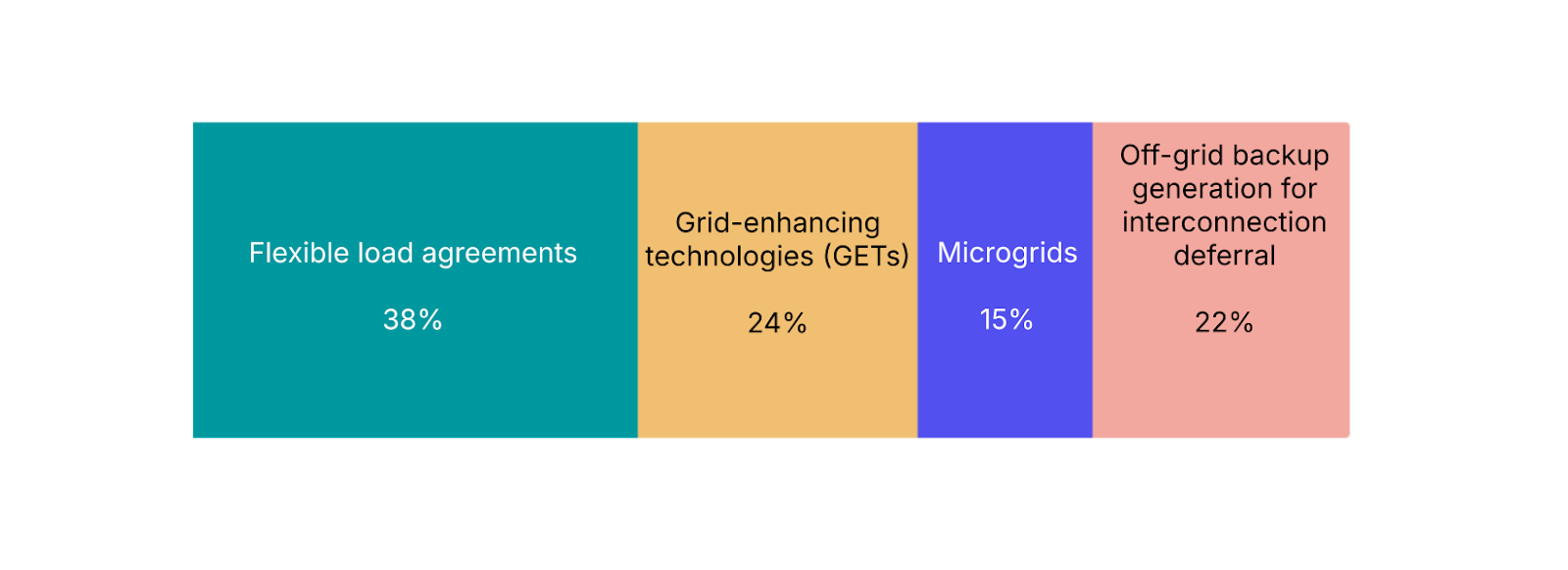

9. Which tech will have the biggest impact on speeding up large-loads?

Results: Flexible load agreements rank highest. This reflects how interconnection delays are being managed in practice, as large customers need to adapt demand profiles for grid constraints.

Expert takes:

“Bring your own capacity/demand flexibility.” - Jigar Shah

“GETs. They're already proven in Europe and ready to be deployed in the US. The cheapest fastest power is what you already have (and aren't using effectively). But the spotlight will probably be stolen by some flashy microgrids.” - Julia Attwood

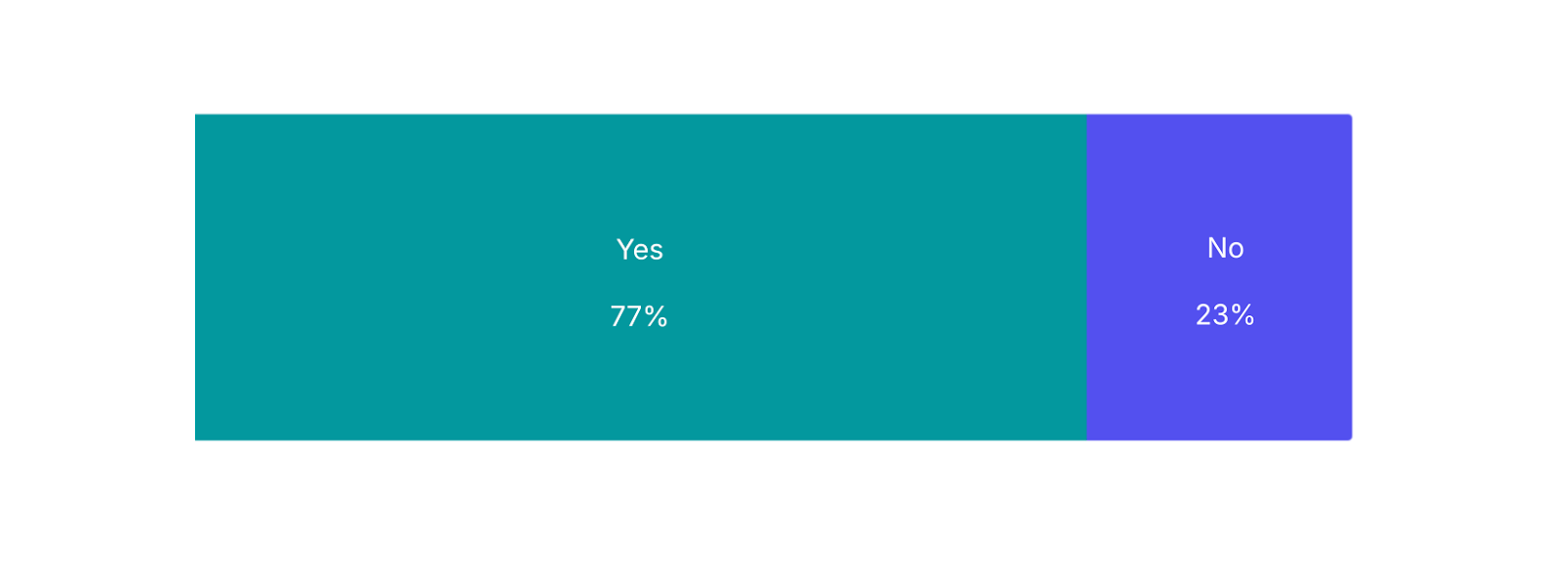

10. Will flexible load programs become standard for new large-load customers?

Results: The majority of you say yes. Flexibility is becoming a default expectation rather than an exception for new large-load interconnections.

Expert takes:

“Major data centers already have 100% backup capacity for reliability. With Ireland already mulling making this a requirement, lots of the most stressed grids could easily follow. Let's just not have a repeat of the Texas bill…” - Julia Attwood

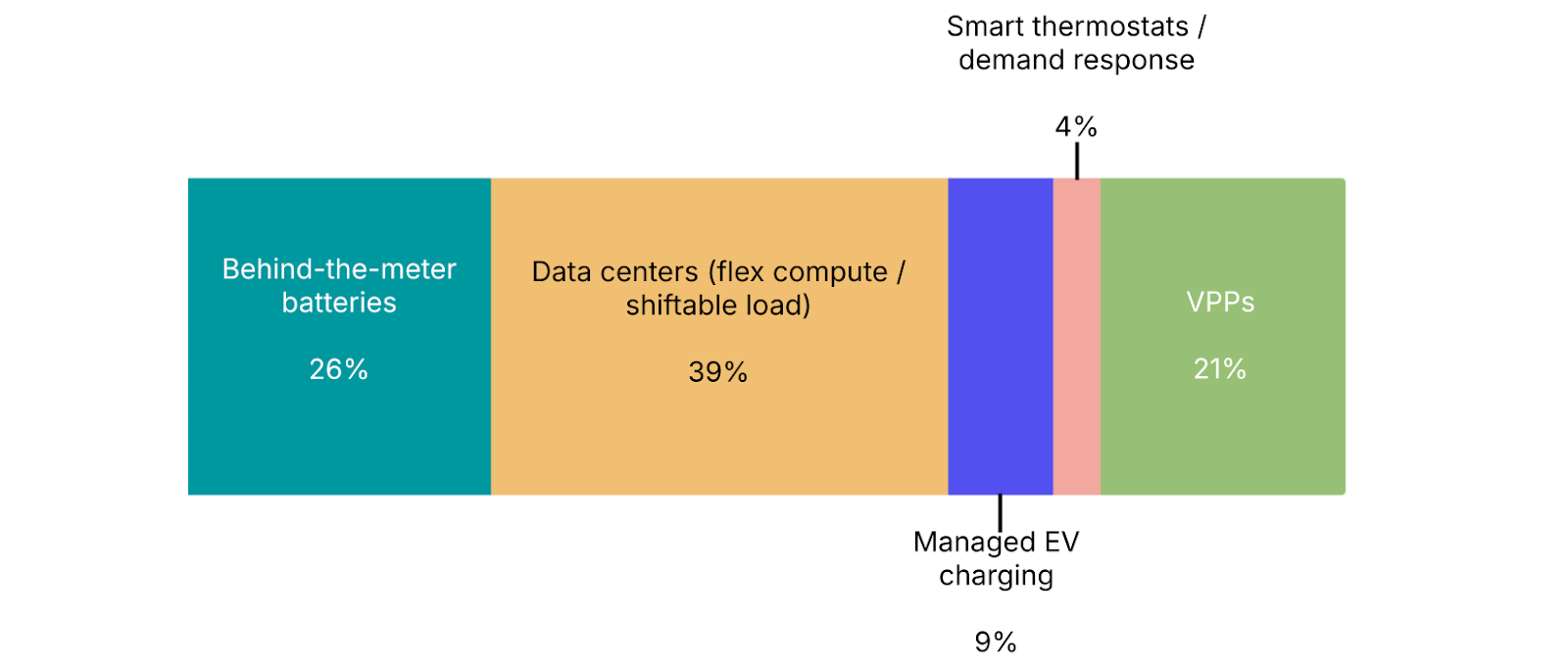

11. Fastest-growing flexible grid asset?

Results: You picked flex compute and shiftable load from data centers. Data centers are increasingly looking to connect to the grid and being good grid citizens is one path forward. Some write-ins included coordinated DERS, energy efficiency, combination, and policy.

Expert takes:

“Virtual power plants. Bonus: in front of the meter large scale batteries.” - Andrew Beebe

“Batteries, followed by Managed EV Charging.” - Jigar Shah

“VPPs – and at least one more state-mandated VPP. Seeing the Virginia Community Energy Act requiring a VPP pilot up to 450MW, others in Maryland, or North Carolina, at least one more state will put a similar law or regulation into place. Legislation introduced in Oregon, California, Illinois, and Massachusetts. It’ll be the year of a lot of things, but VPPs will be one of them.” - Mark Taylor

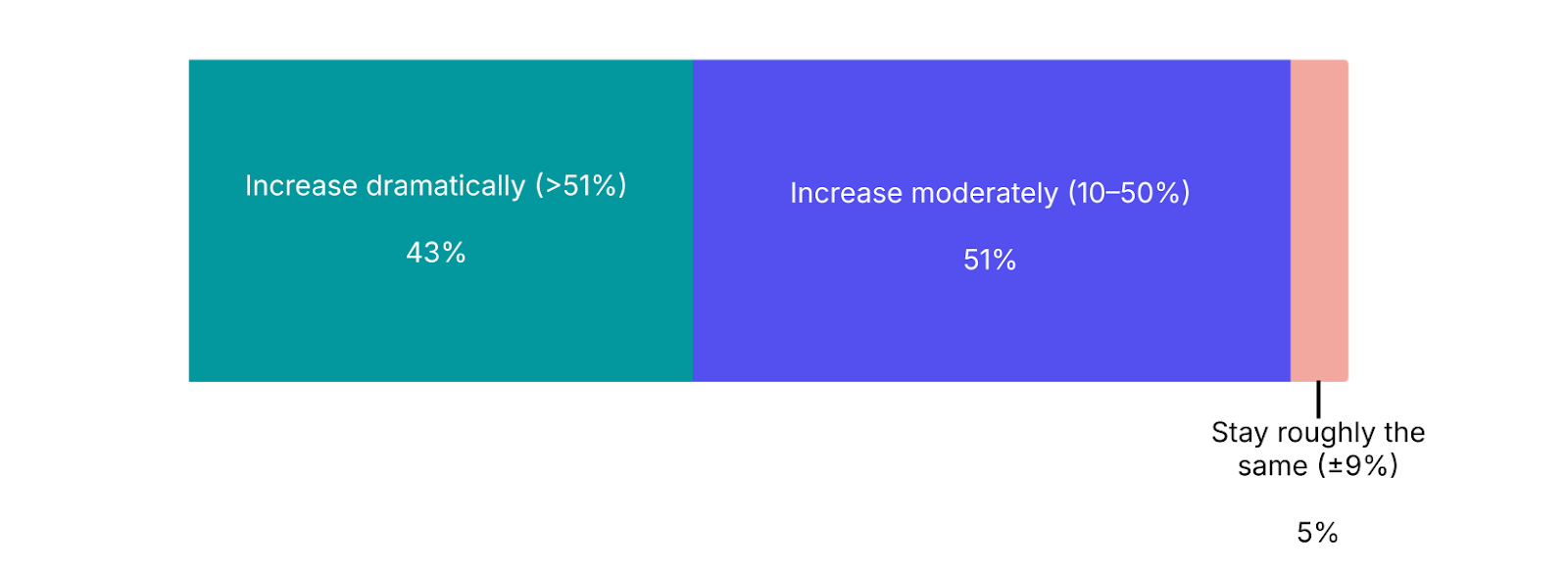

12. Global grid-scale battery installations will...

Results: The majority of you see grid-scale battery installations increasing moderately. Last year, global grid-scale battery installations growth came in at ~38% YoY at the end of November, so that could fit.

Expert takes:

“Dramatically increase, probably double.” - Jigar Shah

“Increase, as fast as possible. The only thing worse than expensive power is no power.” - James Gutman, Strategist, The Carlyle Group

“2026 will be another year of explosive growth for storage installations, driven by the commissioning of multiple multi-gigawatt-hour scale projects in China and the Middle East. This surge in demand is creating intense competition for stationary storage cells, leading more cell manufacturers to switch production lines from producing EV to ESS cells.” - James Frith

13. US electricity prices will…

Results: You foresee a slight increase in electricity prices this year. And indeed, the average electricity price in June 2025 was 6.7% above the rate in June 2024.

Expert takes:

“I believe in 2026 they will keep increasing which will keep pressure on stakeholders to address the price inflation.” - Jeff Johnson

“Is this a trick question?” - Andrew Beebe

“Increase. Objects in motion tend to stay in motion. We need to set (political) expectations accordingly.“ - Dawn Lippert

“Increase due to friction around political challenges.” - Jigar Shah

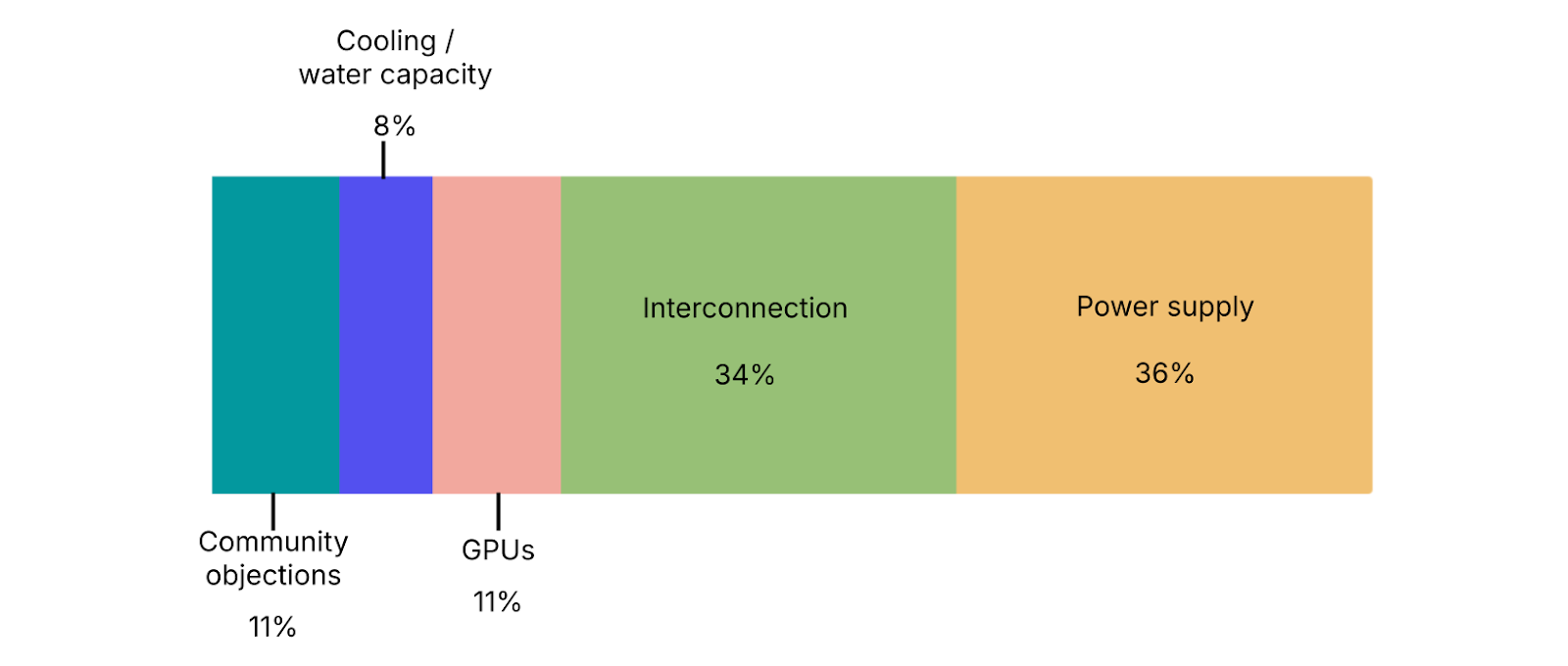

14. The biggest constraint on AI compute expansion in 2026?

Results: A close one, with power supply just eking out interconnection. Physical infrastructure is viewed as the primary constraint.

Expert takes:

“Lack of sustainable infrastructure. Rapidly growing AI compute demand is outpacing the capacity of power grids, water supplies, and data centers. Sustainability and energy availability are becoming limiting factors, with ~$64bn in US data center projects already delayed due to sustainability constraints. Meeting AI-driven compute needs will make sustainable data center infrastructure development a key global priority.” - Lance Uggla, Vice Chairman, General Atlantic, and co-founder, BeyondNetZero

“Power supply and interconnection. GPUs are a constraint, but electricity (and the ability to deliver it at scale and on schedule) is increasingly the limiting factor. In many regions, projects are gated by grid access rather than capital or demand.” - Caie Kelley

“GPUs. If there will be enough GPUs, hyperscalers / developers will find ways to supply the required energy.” - Shira Eting

“The physical constraints are known but the financial constraint is the new bottleneck. Who pays for speed (tariffs, firm service) and who warehouses the development risk? The defining tension of 2026 will be Hyperscalers procuring against product roadmaps vs. Developers/Neoclouds stepping in when utilities won’t sell certainty.” - Shanu Mathew

“Capital. These are becoming asset heavy industries, and if valuations start to reflect this then capital will be rationed.” - James Gutman

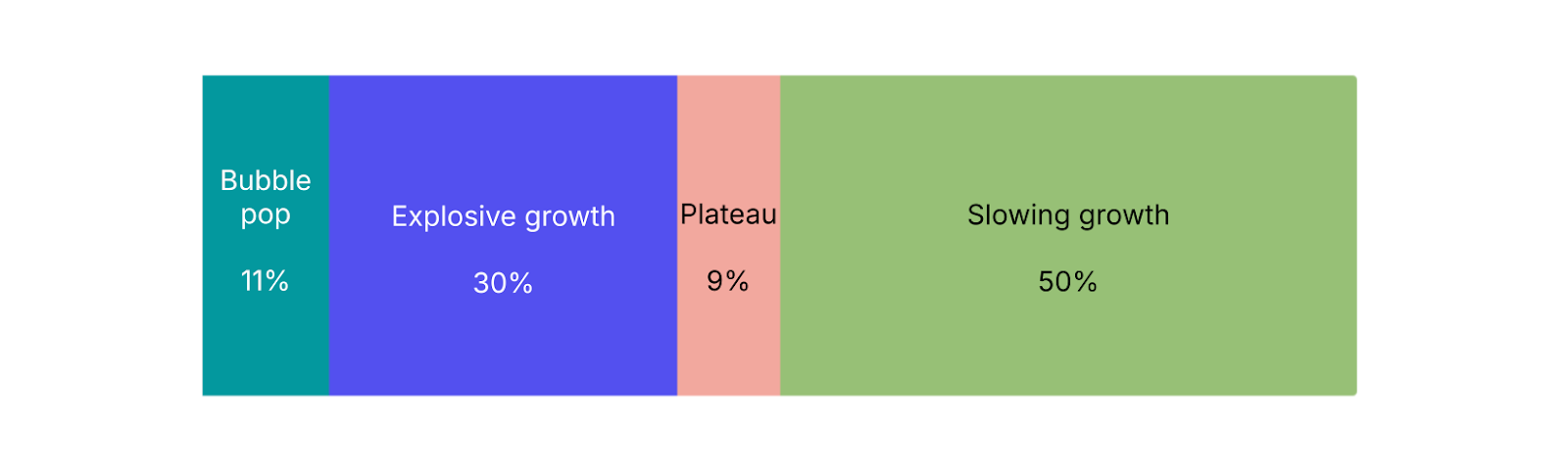

15. Which AI demand scenario will play out?

Results: You said slowing growth. A bit of hedging here, anticipating normalization rather than collapse or acceleration.

Expert takes:

“Scaling laws hold but the market stops rewarding theoretical 2030 GW targets. The capital shifts entirely to execution in the regions that are growing fastest (Tier 1: ERCOT, PJM; Tier 2: SPP, MISO). The only metric that counts in 2026 is: How many GW can you energize in the next 6-18 months?” - Shanu Mathew

“Slowing growth. We’re entering AI’s shift from “infra” to application. If LLM usage consolidates and commoditizes, I expect workloads to swing back from training to inference. This means multi-GW data center clusters built for training will start to level off, and we’ll see smaller, distributed loads closer to where AI is actually being used. The hyperscalers and chipmakers will also innovate around power constraints. Expect to see some major announcements in 2026 on training, chip, or cooling efficiency, potentially DeepSeek-level.” - Kim Zou, CEO & Co-founder, Sightline Climate

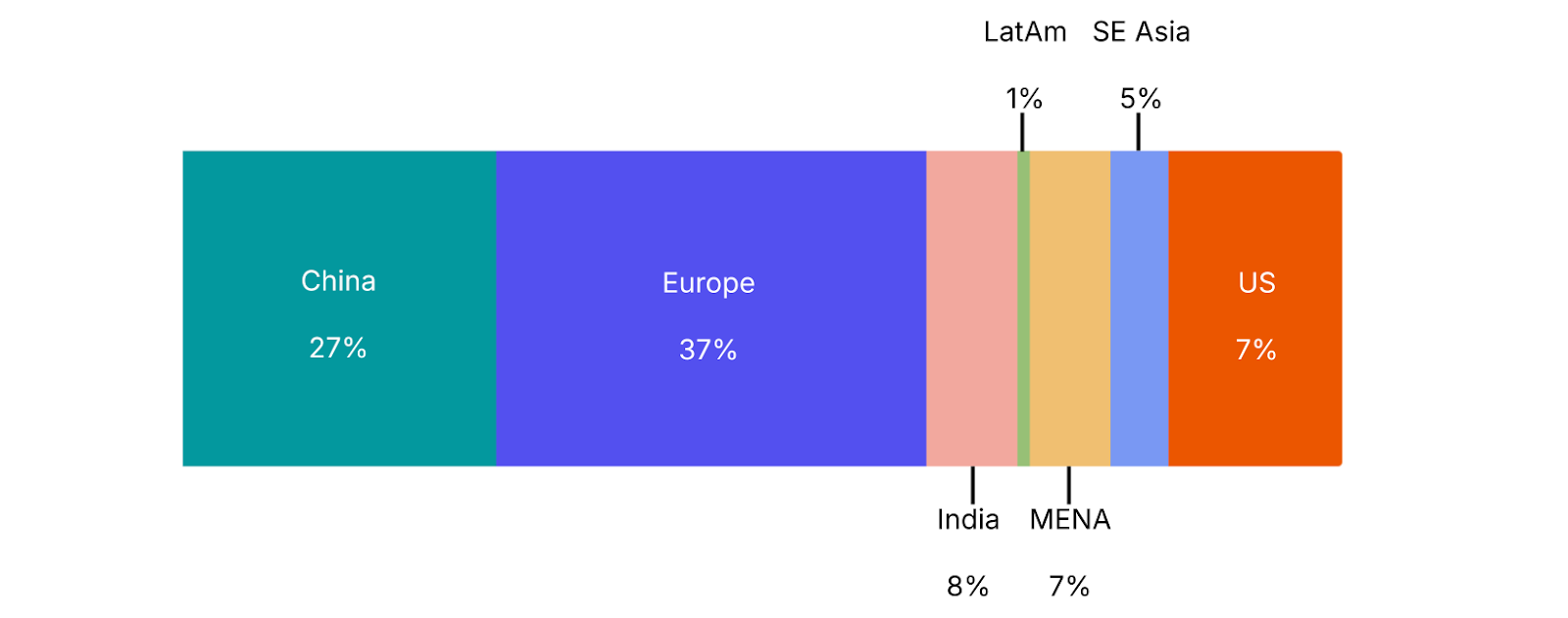

16. Which region will see the fastest climate tech investment growth?

Results: Big bets on Europe here. More than a third of respondents (37%) bet that Europe will see the fastest climate tech investment growth, ahead of China at 27%. You’re expecting favorable policy support, industrial demand, and capital markets to drive new growth.

Expert takes:

“Europe for deal count, China for total investment (depending on how you classify all that state funding). But I'm watching India for exits.” - Julia Attwood

“Singapore on paper, China in reality. Many Chinese companies are opting to move their HQ to Singapore for ease of doing business internationally, but the underlying talent and expertise will remain Chinese. The big three - solar, batteries, EVs - have been led by Chinese expertise, so I think it will be them driving the innovation and deployment behind-the-scenes.” - Kim Zou

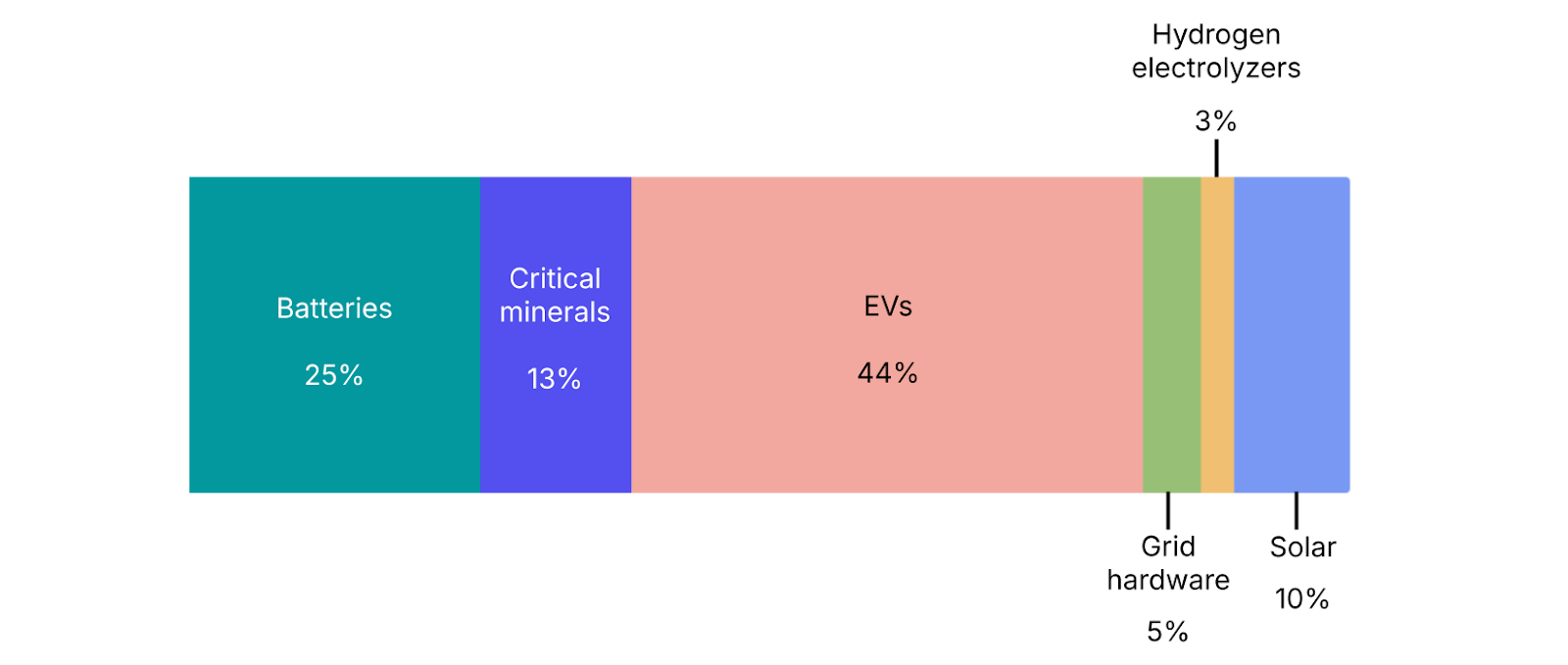

17. Which Chinese export will gain the most global market share?

Results: EVs dominate the bet. And for good reason: China’s EV export volume likely exceeded ~2m units in 2025, almost doubling from the ~1.25m exported in 2024.

Expert takes:

“Batteries of course! But 2026 could be the year of peak Chinese battery exports as cell makers transition to overseas production bases. As part of this transition we can expect to see some big announcements on partnerships between Chinese cell makers and Western companies in 2026.” - James Frith

“EVs and grid hardware. But also: China will be exporting not just products but production capacity.” - Sharon Chen and Roger Zhang

18. Climate tech policy momentum will...

Results: A majority of respondents expect climate tech policy momentum to stay roughly the same. The market is pricing in stasis, not momentum.

Expert takes:

“Dramatic expansion at the state/local level, especially forcing data centers to accept flexibility solutions.” - James Gutman

“It will be a patchwork. We’ll see acceleration for some (minerals, geothermal) and others not able to get out of the mud.” - Dawn Lippert

“Strengthen, though not for climate reasons. Geopolitical frictions are escalating, energy is a (the?) core security issue, and industrial policy is back. Governments will be more active - not less - in finding ways to reduce dependence on imported energy, which for most means fossil fuels.” - James Gutman

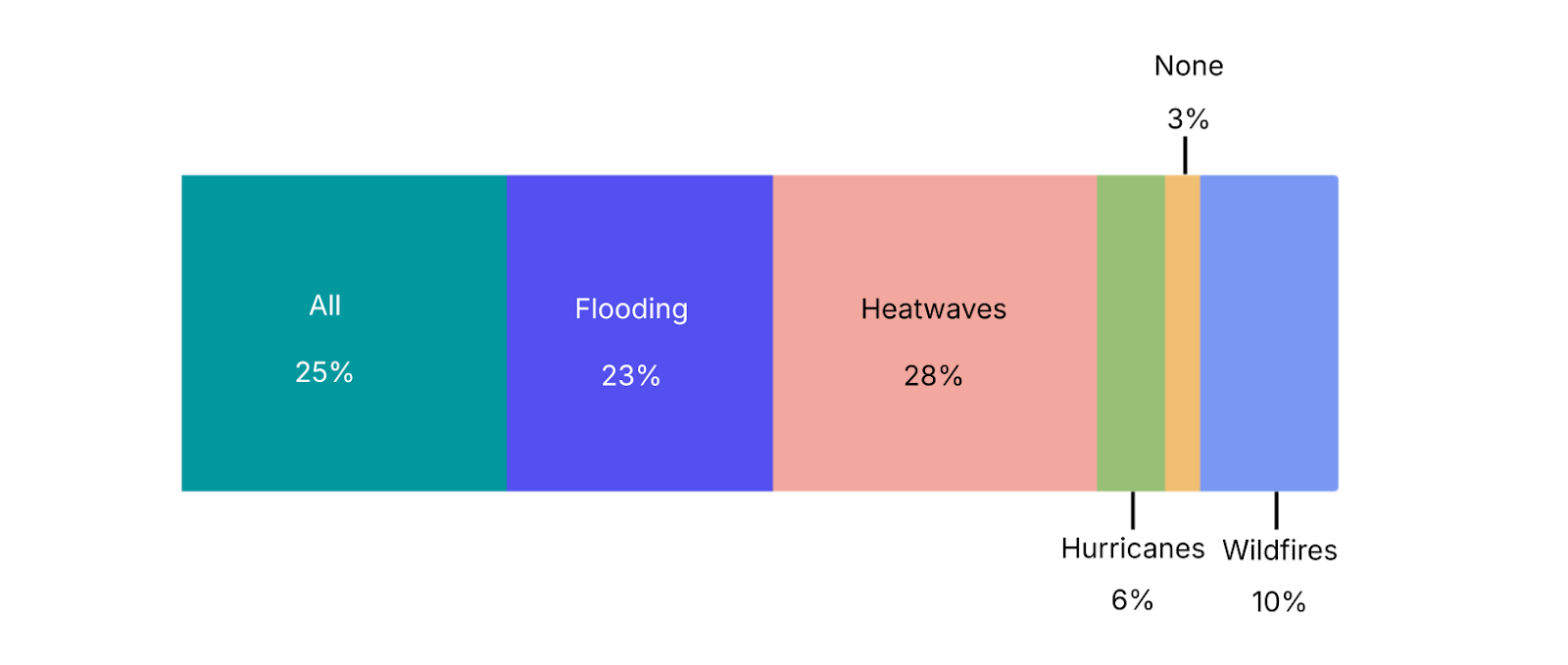

19. Which climate hazard will hit a new intensity record?

Results: You’re betting on extreme heat, but it was a close call with flooding and the catch-all, all of them. And 2025 finished as one of the two hottest years on record, just behind 2024.

Expert takes:

“Heatwaves, but 2025 was a quiet year for US continental landfalls for hurricanes. If that changes in 2026, watch for a rapid rise in adaptation, resilience, and grid investment.” - Julia Attwood

20. Climate adaptation will go mainstream.

Results: The majority of you said that 2026 is the year of climate adaptation. And 2025 did see a dramatic rise in resilience and adaptation-focused investment, according to our recent Investment Trends report.

Expert takes:

“It already has. Adaptation is embedded in insurance underwriting, grid hardening, building retrofits, wildfire mitigation, and municipal infrastructure planning. Companies like Stand and others are selling into buyers responding to real financial exposure. Resilience spending is increasingly treated as core infrastructure investment.” - Caie Kelley

“Not yet, we would need catastrophic event (Covid-like) for that to happen.” Shira Eting

“Has it ever been otherwise? Adaptation is an individual response to a collective problem. It’s what we can control.” - James Gutman

What was so 2025?

What’s the next big thing for 2026?

What were the biggest energy / climate tech wins of 2025?

“The Rise of BYOP/C (Bring Your Own Power/Capacity) to beat the interconnection queue. Large loads stopped treating power as a guaranteed utility service and started treating it as a project finance problem. From bridge power to on-site microgrids, the market is choosing speed + reliability over ideology.” - Shanu Mathew

“Growth (commercial and financial) of energy players such as Fervo and Crusoe. I will also contrarily argue that the ‘fall’ of the voluntary carbon credit markets is a win, as it gets us all focused on what really works economically.” - Shira Eting

“First time clean energy met 100% of all new electricity growth globally. Including solar, wind, nuclear.” - Jigar Shah

“The application of AI to the energy and climate sector has been ongoing, but 2025 emerged as the year when major companies truly scaled up the use of AI to solve practical, climate-related problems. This trend is demonstrated by Percepto's AI-powered drone monitoring for grid assets and Monolith's use of AI to speed up new battery testing and adoption in the automotive industry.” - James Frith

“Solar plus storage. The value is in the battery. The ability to move joules over ever-increasing timeframes unlocks profitability and thus investment.” - James Gutman

“The biggest win was the shift from novelty to execution. 2025 made the real work visible. Interconnection, permitting, and community engagement moved from background details to core parts of building climate companies. Many teams gained a clearer understanding of how infrastructure timelines actually work, and adjusted their plans accordingly..” - Caie Kelly

“The biggest win in my view is having certainty on the OBBB tax bill. The questions about that made investing challenging and having some level of policy settled for the foreseeable future helps allow capital to flow.” - Jeff Johnson

“2025 saw strong momentum in several sectors, especially those touching on domestic supply chains, data centers, and energy dominance. In our Elemental and Earthshot portfolios, think critical minerals (KoBold Metals), geothermal (Fervo Energy), energy storage (Energy Dome), and anything AI-meet-infrastructure (Emerald AI).” - Dawn Lippert

“In 2025, the clean energy and manufacturing industry proved it can scale through headwinds and uncertainty. Even amid changing policy incentives, private capital continued to flow -- particularly through the transferable tax credit market, which more than doubled in size from 1H2024 to 1H2025 and cemented itself as a lasting key lever of clean energy project financing. We saw real momentum in technologies that support grid reliability, like energy storage, and onshoring upstream supply chain.” - Alfred Johnson

“Big nukes are back, baby! (See 3 Mile Island, but also all of the other re-commissions happening). Everything electric (non-US version). From Norway to China to *Vietnam*, everyone else is going electric, except us and maybe Russia. And geothermal. Hotter than ever, you dig?” - Andrew Beebe.

“Mainstream adoption. Over 90% of new power capacity added is renewable. These milestones show the energy transition has moved from promise to scale, with new solutions winning on cost, speed, and deployment.” - Lance Uggla

“Solar continues to deploy despite headwinds. More urgency of a drive towards firm (though maybe less clean) power - geothermal, nuclear, storage, grid infra. In China: Large demo projects in green fuels, nascent carbon market signaling pressure on heavy industrial players.” - Sharon Chen and Roger Zhang

What were the biggest losses?

“Electricity’s 'Affordability Crisis' Moment. Electricity prices have officially entered the national affordability conversation. Whether driven by grid capex, higher peaks, or load growth, the bill impact is now the primary political constraint that can kill projects and new policy alike.”- Shanu Mathew

“Trump’s OBBA’s impact on solar, wind, and hydrogen.” - Shira Eting

“Disruption in the US/DOE had a major chilling effect on the enthusiasm for funding hard-to-abate sectors.” - Jigar Shah

“The loss of the EV tax credit under the IRA had a huge impact on the clean energy sector. However, the retention of key provisions — specifically the 45X battery manufacturing tax credit and the investment tax credit for stationary storage systems — offers a silver lining, actively driving the localization of battery manufacturing and growth in the stationary storage market within the US.” - James Frith

“Policy stability. Investors (should be able to) treat policy as a given and make economic decisions accordingly. That is why industrial policy works when it does. An erratic policy landscape invites rent-seeking and exacerbates mal-investment.” - James Gutman

“Time and coordination. Interconnection queues, permitting, and local engagement became central to execution, and teams that internalized that early are now better positioned. The industry learned faster ways to plan around real-world timelines rather than idealized ones.” - Caie Kelly

“The biggest loss in my view is the continued lack of civil engagement across ideological lines on how to achieve American and wider Western leadership in the energy sector. We continue to have so many advantages in terms of innovation and capital, but we aren’t channeling it effectively nor pushing forward on permitting reform to create a field for all energy technologies that should win to be able to do so.” - Jeff Johnson

“The biggest loser was US climate innovation. We lost ground to countries investing in technology innovation across the board - even if some sectors gained ground. Many promising companies, even those hitting their milestones, struggled to raise capital. Another loser is FOAK funding; in a survey we conducted with Sightline, 69% of respondents expected FOAK capital availability to shrink further through 2026, and from our conversations with entrepreneurs, this held true.” - Dawn Lippert

“Reduced policy support for established climate technologies like wind and solar was a setback to the sector, especially in light of rising energy demand and declining affordability. But that doesn’t mean the sector stalled. Solar has proven resilient, particularly when paired with storage, and we are seeing increased investment into other areas of innovation, including geothermal and advanced nuclear.” - Alfred Johnson

“The biggest loss was time. In 2025, policy uncertainty around the energy transition in some geographies caused investor hesitation, resulting in delayed capital deployment and preventing several high-quality, scalable businesses from securing the funding needed to reach commercial maturity.” - Lance Uggla

“Wind in the US; Uncertainty in policy-dependent markets (hydrogen, heavy industry, maritime decarb).” - Sharon Chen and Roger Zhang

What are we leaving behind in 2025?

“Energy tribalism (e.g., solar only, gas only, nuclear only, etc.). It's increasingly abundant in an era of load growth, many generation types will be required and each plays a different role in a stable, clean, affordable, and reliable system. We should leave behind zero-sum thinking and find ways to work together vs. against each other. Systems thinking will win.” - Shanu Mathew

“Most of the voluntary carbon credit-based businesses, alternative proteins.” - Shira Eting

“Focus is moving away from technology innovation being an endpoint to affordability through deploying solutions already at scale.” - Jigar Shah

“Our illusions.” - James Gutman

“We’re leaving behind the idea that proving the technology is the finish line. In deep tech, technical progress is table stakes. What matters is whether a company can manufacture, deploy, finance, and operate inside complex systems over long time horizons..” - Caie Kelly

“Peak uncertainty. We are likely permanently living with more uncertainty than the past, but the extra heightened uncertainty from the initial tariff rollout and tax bill has subsided.” - Jeff Johnson

“The green premium. The best companies will win on cost, speed, and user experience.” - Dawn Lippert

“We’re leaving behind the idea that clean energy rises or falls on policy alone. The tailwinds in this market -- including surging energy demand from data centers and consumers, rising utility rates, the return to onshore manufacturing, and a critical need for massive investment to build and deploy new energy infrastructure -- started before 2025 and will continue well beyond 2026.” - Alfred Johnson

“The phase of climate investing driven more by narrative than fundamentals. Capital is growing more discerning, and the market is increasingly rewarding companies with demonstrated customer demand, credible unit economics, and scalable business models, rather than those driven by ambition and good intentions alone.” - Lance Uggla

“China is trying to put brakes on bloody price wars and consolidate overcapacity. This means a floor may finally materialize on prices in solar, batteries, and EVs - we are leaving behind continued Capex cost-down on mature renewable technologies.” - Sharon Chen and Roger Zhang

“Being stuck in the past. The pendulum will swing back (it always does). But there’s no point in holding onto what could have been on net zero and decarbonization targets. We have a new reality in climate (slowing policy momentum) and energy (growing demand) and we need cheaper, better, cleaner solutions that pencil out in the state of the world we’re in today. Let’s get to work.” - Kim Zou

.jpg)

.jpg)

.png)

.png)